Merchant cash advances (MCAs) offer fast funding — typically within a few days — and a straightforward application that usually requires nothing more than a few months of bank statements.

Cleaning businesses commonly use merchant cash advances to cover urgent expenses, such as:

- New equipment

- Payroll gaps

- Cleaning supplies and last-minute restocks

- Additional staff during peak season

- And more

We’ll compare merchant cash advances to conventional bank loans, where you have to wait 30 to 60 days for funding and must prepare mountains of paperwork to apply.

Despite the benefits, the offer you choose is the single most important decision you’ll make when applying for a merchant cash advance. It’s the difference between securing competitive rates and getting locked into expensive terms.

This guide covers how merchant cash advances work, what it takes to qualify, and how to prepare and apply for one. Most importantly, it shows how to identify and avoid low-quality MCA lenders and secure the lowest possible rates (you can skip ahead to that section here).

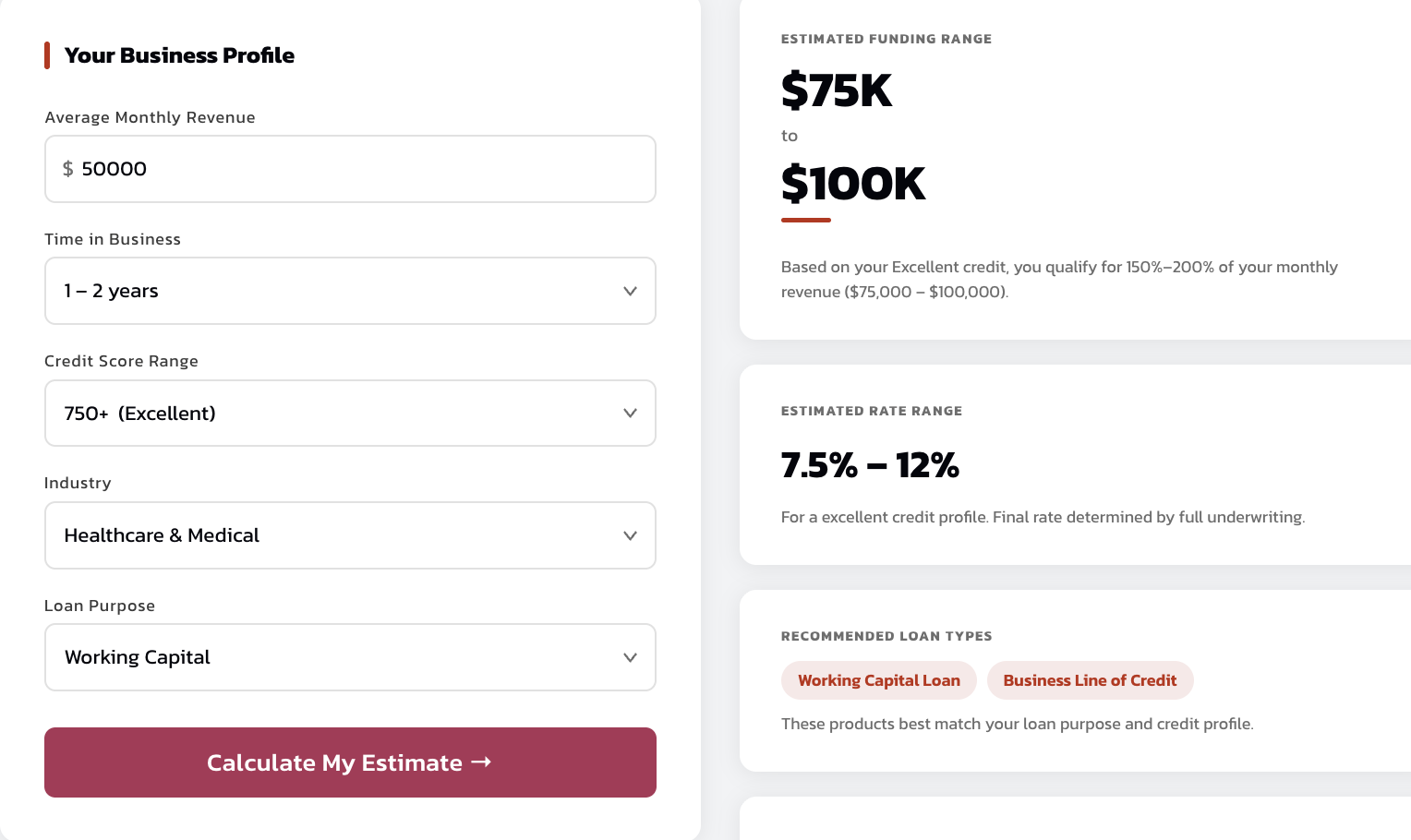

Use our MCA calculator to generate instant quotes and find out what loan amounts and terms your cleaning business can qualify for.

How Merchant Cash Advances Work and the Benefits They Offer Cleaning Businesses

A merchant cash advance involves a lender wiring a lump sum into your business bank account, typically 100% to 200% of your monthly revenue. The lender then automatically deducts a percentage of your revenue via ACH, or in some cases, a percentage of your daily credit card and debit card transactions, until it’s fully repaid.

The main advantages of a merchant cash advance are how easy it is to qualify and how quickly funds hit your bank account. Most MCA lenders keep their requirements simple, only asking for a minimum monthly revenue and a minimum time in business. The exact numbers vary by lender, but meeting those two criteria is generally enough to qualify.

Contrast those eligibility requirements to large banks that want perfect credit, hard collateral, cash reserves, strong profit margins, and more.

Because MCAs don’t evaluate your entire financial profile, they also fund significantly faster than banks. Most MCAs are in your account within 3 to 5 business days, and the fastest MCA providers like Redline Capital can fund as quickly as 4 hours.

The main disadvantage of a merchant cash advance is that they are pricier than bank loans and have shorter repayment periods. That said, later in this article, we cover how to find MCA lenders offering the lowest rates so you can reduce some of those added costs.

Requirements to Qualify for a Merchant Cash Advance

The requirements to qualify for a merchant cash advance will depend on the lender.

For example, some MCA lenders work with small cleaning businesses and solopreneurs. They may only ask for a couple of thousand dollars in monthly revenue and an operating history of 3 to 6 months. Others work with more established cleaning companies and can fund much larger amounts.

At Redline Capital, we work with businesses of all sizes. We only have three requirements, making it possible for most cleaning companies to qualify:

- $30,000 in monthly revenue

- A 12-month operating history

- A U.S.-based location

We don’t require a minimum credit score, collateral, or a spotless credit profile.

Given how simple our qualification criteria are, the only documentation we need is four months of bank statements confirming your monthly revenue. No tax returns, balance sheets, accounts receivable reports, or proof of insurance.

If you qualify, you’ll have offers in your inbox within an hour and funds in your bank account today or tomorrow. We can also handle emergencies. For example, a cleaning business recently had two pressure washers break down mid-job, and we funded them within four hours.

Here’s what business owners say about working with us:

How to Apply for a Merchant Cash Advance with Redline Capital

Our online application process is straightforward and takes less than a minute to complete.

- Get your estimated advance amount and rate upfront with our MCA calculator. Simply enter your monthly revenue, time in business, credit score range, and industry.

- Submit four months of business bank statements. That’s the only document we need.

- We review your monthly revenue and run a soft credit check. Bad credit does not disqualify you; we just use it to determine the rates you qualify for.

- You receive multiple offers within an hour, each containing the advance amount, factor rate, total payback amount, payment frequency (weekly or monthly), and term length.

- Take your time reviewing our offers. We encourage you to shop around and compare our offers to those of other MCA lenders.

- You receive funds the same day you accept an offer.

How to Secure the Best Cash Advance Rates for Your Cleaning Business & Avoid Predatory Lenders

Consider Whether They Are a Direct Lender or a Broker

A common assumption among business owners is that applying directly to a lender means better rates, since there are no broker fees involved.

While this is true for lower-quality brokers, applying with a high-quality broker can actually help you secure better offers than applying on your own, largely because of the deal volume they send to lenders.

For example, at Redline Capital, we’ve built relationships with our lending partners (e.g., OnDeck, Headway Capital, Rapid Finance) over the past decade by sending them hundreds of millions of dollars in loan applications. That volume helps grow their business, and they reward us with wholesale rates, larger loan amounts, and discounts that wouldn’t otherwise be on the table.

When you apply through us, you’re leveraging the collective business we’ve sent our lending partners to access pricing that individual applicants simply don’t get.

Lower rates aside, there are a few more advantages to working with a high-quality broker like Redline Capital:

- With a single application, we submit your file to multiple lenders simultaneously and bring back competing offers for you to compare. You see the range of financing options available without having to apply to each provider separately.

- When a cleaning business faces a true emergency, we don’t route them through a standard application process. We reach out directly to loan officers we know personally at our lending partners. That’s how we’ve delivered funds in just four hours.

Check Whether They Have Experience Funding Cleaning Businesses

To an underwriter with no industry experience, a cleaning business can look risky on paper. Revenue can spike suddenly when a large commercial contract comes in and drop when a client churns. Payroll costs are also high relative to margins, and accounts receivable can age out when corporate clients run slow on invoicing cycles.

Lenders who don’t know the cleaning industry often read those patterns as instability and end up charging higher rates.

At Redline Capital, we’ve been financing cleaning businesses for over a decade. We understand that, for example, a revenue dip in January doesn’t signal a struggling business — it means the post-holiday commercial deep-clean cycle has wound down.

That context and industry experience means we won’t inflate your rates over financial patterns that are completely normal for cleaning businesses.

Do They Aggressively Pressure You Into Accepting Their Offers?

We’ve noticed that MCA lenders who are most aggressive about following up after an application tend to have the worst offers. They know their offers aren’t competitive, so they want you to accept before you’ve had a chance to compare them to what else is available.

As a result, we recommend avoiding lenders who pressure you to accept their offers.

At Redline Capital, we never pressure you to accept our offers. We actively encourage you to shop around, get quotes from other providers, and put them next to what we’ve sent you. Our rates hold up under comparison, and we’d rather earn your business by being the best option than by making it difficult to look at alternatives.

Secure a Same-day Cash Advance for Your Cleaning Business with Redline Capital

Submit four months of bank statements to see what you qualify for.

Alternatives to a Merchant Cash Advance

While a merchant cash advance works well for cleaning businesses that need fast capital and can’t meet bank eligibility requirements, it isn’t the right financing solution for everyone. Here are the main alternatives worth considering.

Bank Loans

Bank loans are the most common form of small business loans because they offer low interest rates and long repayment terms.

For a cleaning business with strong financials and time to spare, a bank loan is a cheap way to access business funding. The total cost of borrowing is lower, the repayment period is longer, and the monthly payment is predictable.

However, traditional banks are risk-averse lenders with qualification criteria that make it difficult for most cleaning businesses to qualify. They typically want a personal credit score of at least 720, two or more years of operating history, collateral — including real estate, equipment, or other hard assets — and a complete documentation package including tax returns, profit-and-loss statements, and balance sheets.

Due to banks’ strict underwriting standards, only about 13% of small business owners are approved.

Best for: Established cleaning businesses with excellent credit, clean financials, hard assets to pledge, and business needs that aren’t urgent.

SBA Loans

An SBA loan is a traditional loan that’s partially guaranteed by the Small Business Administration, meaning if the borrower defaults, the government covers a percentage of the outstanding balance. This reduces risk and allows lenders to offer lower interest rates, longer repayment periods, and smaller down payments.

The SBA 7(a) is the go-to choice for cleaning businesses because it can be used to cover working capital, equipment, and expansion.

The tradeoff is that SBA loans are even more strict and paperwork-intensive than standard bank loans. Lenders require tax returns, financial statements, a business plan, and documentation about how you intend to use the funds. Cleaning businesses with seasonal revenue swings or limited operating history often struggle to meet SBA eligibility requirements, even when their business is genuinely healthy.

Best for: Cleaning businesses that are financially strong, have been operating for at least two years, and are planning ahead — expansion, purchasing equipment, refinancing — rather than addressing an urgent cash need.

Invoice Factoring

Invoice factoring is a financing arrangement where you sell your outstanding invoices to a third-party company in exchange for immediate cash. The factoring company advances you a percentage of the invoice value and takes over the job of collecting payment from your client. Once your client pays, you receive the remaining balance minus the factoring fee, which generally runs between 1% and 5% per invoice.

For cleaning businesses with commercial clients on net-30 or net-60 payment terms, factoring can be a practical way to turn completed work into cash without waiting for invoices to clear. The approval process is based primarily on your clients’ creditworthiness rather than your own credit profile, making it accessible to businesses that might not qualify for conventional financing. Because you’re selling a receivable rather than taking on new debt, it also doesn’t add a loan obligation to your balance sheet.

However, invoice factoring requires you to hand over control of collections to a third party. This can strain client relationships, particularly if the factoring company takes an aggressive approach to collections.

Best for: Cleaning businesses with a reliable base of commercial clients on extended payment terms who need to convert completed work into immediate cash.

Equipment Financing

Equipment financing is a loan or lease specifically for purchasing business equipment, with the equipment itself serving as collateral. For cleaning businesses, this covers commercial-grade vacuums, floor scrubbers, carpet extractors, pressure washers, steam cleaners, and any other high-cost tools.

Because the equipment secures the loan, lenders take on less risk and can offer more competitive rates than unsecured loans. You can acquire the equipment your business needs without depleting your working capital, and you don’t have to pledge personal assets or other business property.

But the process takes longer than an MCA. Lenders require vendor quotes, equipment appraisals, and documentation before approving a loan. The funds are also restricted to equipment purchases, so unlike a business cash advance, you can’t use them to simultaneously cover equipment, payroll, and rent.

Best for: Cleaning businesses that need to purchase or replace specific equipment and want to spread the cost over time at a lower rate.

Business Line of Credit

A business line of credit gives you access to a set amount of funds you can draw from whenever business expenses arise. Unlike a cash advance or a term loan, where you pay interest on the entire lump sum, lines of credit only charge interest on the amount you use.

For cleaning businesses, a line of credit is particularly well-suited to managing the recurring timing gap between when expenses hit and when clients pay. If payroll is due on Friday and a commercial client’s invoice doesn’t clear until the following week, you draw from the line to cover the shortfall, then repay once the payment arrives. The credit resets and becomes available again for the next cycle.

However, qualifying for a line of credit is more demanding than qualifying for an MCA. Most lenders look for an established credit history and a solid operating track record, and some require collateral. Credit limits may also fall short for larger, one-time capital needs.

Best for: Cleaning businesses with solid credit that need ongoing, flexible access to capital for recurring cash flow gaps, rather than a one-time lump sum for a specific expense.