Plumbing businesses face significant cash flow challenges because they must cover job costs like labor, materials, and other operating expenses upfront, then wait weeks for clients to pay.

Traditional bank loans may seem like the obvious financing solution to bridge this cash flow gap. However, banks often take around 30 to 90 days to fund loans, which is longer than most clients take to pay.

Funding speed aside, banks have steep requirements that make it difficult for most plumbing companies to qualify. They typically want years of audited tax returns, near-perfect credit scores, hard collateral like real estate or equipment, a business plan, strong profit margins, and cash reserves.

That’s why merchant cash advances (MCAs) have become a go-to business financing option for plumbing businesses. Unlike traditional bank lenders, MCA lenders don’t evaluate your entire financial profile but instead focus on your business’s monthly revenue. No financial statements, collateral, or credit score minimums.

This has a few key advantages for plumbing businesses:

- Faster access to capital. Because MCA providers only review your monthly revenue, and not your entire financial profile, they can fund within a few days. Some can even fund on the same day or the next.

- Easier to qualify. Revenue is the primary requirement, so if your business clears the MCA lender’s revenue bar, you qualify. Plumbing contractors that fail to qualify for bank loans often qualify for an MCA without issue.

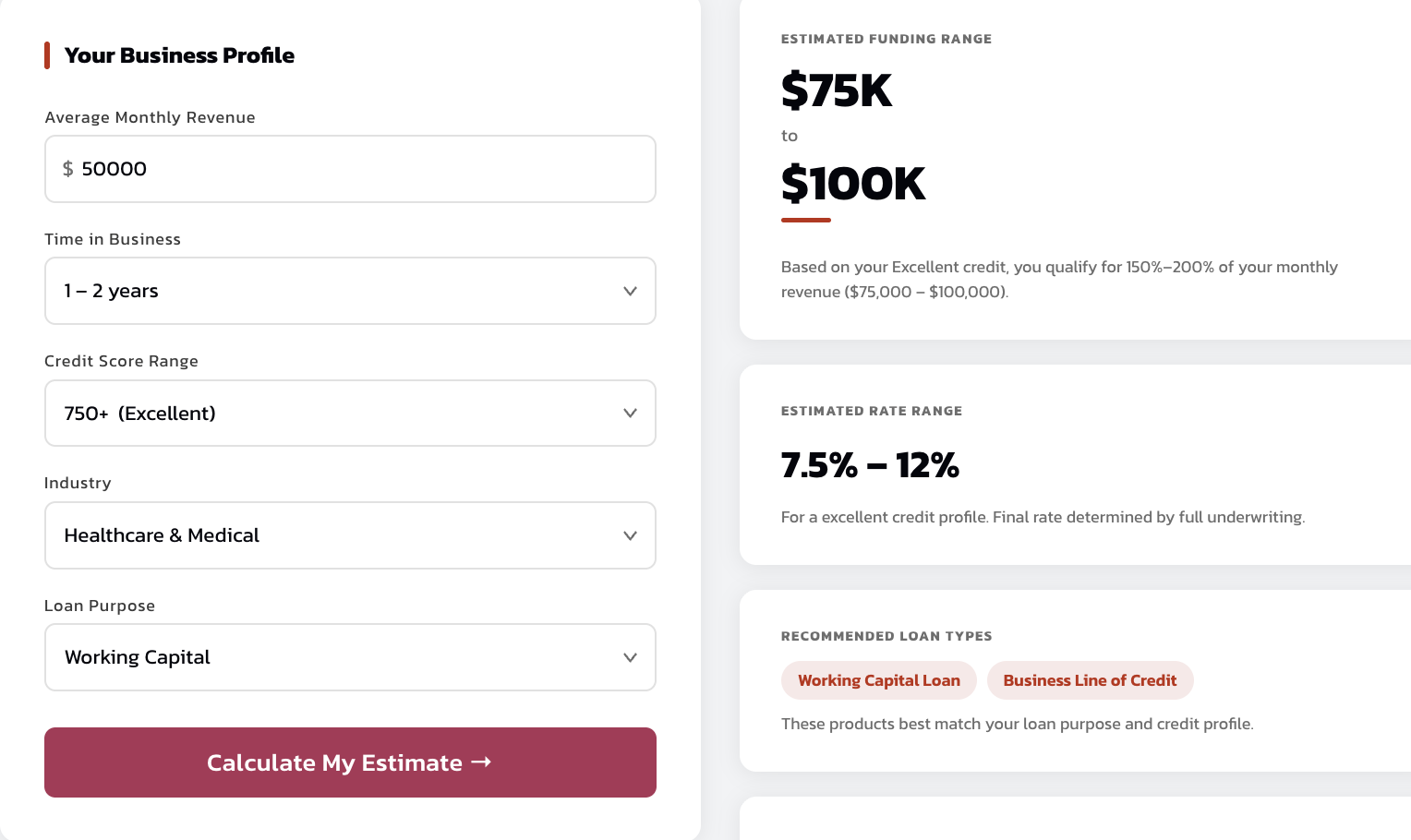

- Larger advance amounts. MCA providers don’t limit how much you can qualify for based on your collateral, cash reserves, or any other factors banks consider. So, borrowers are often surprised by how much they can qualify for. At Redline Capital, for example, businesses commonly qualify for 150% to 200% of their monthly revenue, while banks usually lend up to 50%.

- No collateral required. Merchant cash advances don’t require vehicles, equipment, or personal assets as collateral, reducing your borrowing risk.

This guide covers how merchant cash advances work for plumbing businesses, what it takes to qualify, the steps involved in applying, and what to look for in a lender.

We also review some alternatives at the end, including small business loans, SBA loans, and a business line of credit, since a cash advance isn’t the right fit for every situation.

Use our MCA calculator to see what advance amounts, rates, and loan terms your plumbing business qualifies for.

How Merchant Cash Advances Work for Plumbing Businesses

A merchant cash advance is a short-term business funding solution assessed and approved based on your business’s monthly revenue, not your entire financial profile. As a result, most MCA lenders only need a few months of bank statements to confirm your monthly revenue, and can fund within a few days.

The MCA lender wires a lump sum of approximately 150% to 200% of your monthly revenue into your business bank account, and you repay a percentage of your revenue until the balance is cleared. Plumbing businesses use these funds for a range of capital needs, including purchasing materials before a large job, covering payroll, replacing broken equipment, or handling day-to-day business expenses that can’t wait for a client invoice to clear.

The pricing of an MCA also differs from that of a traditional bank loan. MCAs price their terms using factor rates and not interest rates. A factor rate is a fixed number applied to your borrowed amount that determines the total you’ll repay.

For instance, if you receive $100,000 with a 1.15 factor rate, you repay $115,000 in total. That amount is fixed from day one; it doesn’t accrue or change based on how long it takes you to pay it off.

Merchant Cash Advance Requirements for Plumbing Businesses

Different MCA lenders have different requirements, but at Redline Capital, we only ask that your plumbing business generates $30,000 in monthly bank deposits.

Our simple eligibility criteria make it easy for most plumbers to qualify. To illustrate this, we have an 80% borrower approval rate, while banks approve only about 13% of applicants.

The only document we ask for is four months of business bank statements showing your revenue. No tax returns, profit-and-loss statements, balance sheets, or business plans required.

How to Apply for a Merchant Cash Advance

Applying for a cash advance with Redline Capital takes a few seconds via our online application, and you receive funds in your bank account on the same day you apply.

Here’s what the entire application process looks like:

- Run your revenue numbers through our MCA calculator to get an estimate of the loan amount and rate you can qualify for.

- Submit four months of bank statements. This is the only document we require. It shows us your monthly revenue, which is everything we need to assess your application.

- We analyze your bank deposits and run a soft credit check. Bad credit does not affect your eligibility. We only use your credit history to help determine your rate and repayment terms.

- You’ll get multiple offers in your email inbox within an hour, which you can compare side by side. Each offer shows the advance amount, factor rate, total repayment, monthly payments or weekly payment frequency, and loan terms.

- Choose the offer that best suits your specific business needs. Unlike many MCA providers, we never put pressure on you to accept our offers. We actively encourage you to compare what we send with other lenders’ funding solutions before making a decision.

- Receive funds the same day. Once you choose an offer, you get the advance in your bank account within a few hours.

Why Choose Redline Capital Over Other MCA Providers

Most MCA providers can fund within a few days. Here’s what differentiates Redline Capital from everyone else.

We Help You Secure The Lowest Possible Rates

Plumbing businesses consistently secure lower rates with Redline Capital than they do with other MCA providers.

That’s because we’re a broker who has delivered hundreds of millions in loan volume to our lending partners, including OnDeck, Rapid Finance, and Headway Capital, among others. Our partners reward that volume with wholesale pricing, discounted rates, and more flexible repayment terms that aren’t available to businesses applying on their own.

Applying through Redline means tapping into all the business we’ve sent our lending partners over the past 10 years to secure lower rates.

Beyond lower rates, our lender relationships offer two more advantages:

- Submit one application and receive multiple offers. We submit your file to multiple lenders at once and return competing loan options for you to compare side by side. You see the full range of available financing options without having to fill out separate applications with multiple providers.

- Emergency funding available. Because we know loan officers working at Headway Capital, OnDeck, and our other lending partners, we can call them directly for a quote rather than submitting an entire application on the lender’s website. This leads to faster funding than even other MCA lenders. For instance, we’ve helped plumbing businesses settle urgent business expenses on the weekend in under 4 hours.

We Have Over a Decade of Experience Working with Plumbing Businesses

Plumbing businesses have financial patterns that look risky to lenders new to the plumbing industry.

For example, emergency call volume spikes in January when pipes freeze and drops in the summer when residential demand softens. Spring picks up again as construction activity resumes.

To a lender unfamiliar with plumbing, those swings look like instability rather than a normal part of running a plumbing business, causing them to charge higher factor rates and fees. We’ve seen the same pattern with HVAC businesses and other trade contractors. Any service business with seasonal demand gets misread by lenders without industry experience.

At Redline Capital, we’ve been financing trade businesses, including plumbing companies, for over a decade. We understand the difference between a business with seasonality and one that’s actually struggling.

Because of this experience, we won’t penalize you with inflated rates for seasonal patterns or project-based revenue cycles that are standard across the plumbing industry.

We Are Professional and Never Pressure Businesses to Accept Our Offers

MCA lenders who push hardest after you apply tend to have the most expensive rates and loan products. They rely on pressure tactics like repeated calls and emails, along with manufactured deadlines that make it seem like their offers are about to expire. The goal is to get you to accept before you’ve had a chance to shop around.

At Redline Capital, we send your offers and step back. We encourage our clients to shop around because we’re confident our terms are among the most competitive available — and we want you to confirm that for yourself, not feel rushed into a decision.

Here’s what business owners say about our rates and funding speed:

Secure a Fast and Affordable Cash Advance for Your Plumbing Business with Redline Capital

Generate instant quotes using our calculator and see what your plumbing business qualifies for.

Or, you can submit four months of bank statements and have offers in your inbox within an hour.

Alternatives to a Merchant Cash Advance

Invoice Factoring

Invoice factoring lets you convert outstanding invoices into immediate cash by selling them to a third-party factoring company. The factoring company advances a percentage of the invoice value — typically 70% to 90% — and takes over collecting payment from your customers.

Once your customers pay, you receive the remaining balance minus the factoring fee, which typically ranges from 1% to 5% per invoice.

For plumbing businesses that do significant commercial work, this can be a practical way to close the gap between completing a job and getting paid. Approval is based primarily on your customers’ creditworthiness rather than your own financials, making it accessible to businesses that might struggle to qualify elsewhere.

The main limitation of invoice factoring is that you give up control of collections. This can be problematic, especially if the factoring company takes an aggressive approach with your customers.

Read more: Top 6 Accounts Receivable Financing Companies

Traditional Bank Loans

Banks offer the most competitive interest rates available to small businesses, but the eligibility bar is high and the process is slow.

To qualify, most banks want a personal credit score above 700, at least two years of operating history, hard collateral, and a complete documentation package: tax returns, profit-and-loss statements, balance sheets, and a business plan. The approval process typically runs 60 to 90 days, and only about 13% of small business loan applications get approved.

A plumbing business loan from a bank makes sense if you’ve been in operation for several years, your credit is strong, you have assets to pledge, and you’re planning ahead for growth rather than responding to an immediate expense. In that scenario, the lower interest rates make bank financing the cheapest long-term option available.

However, if you need to cover payroll this week, replace broken equipment, or bridge a cash flow gap while waiting on invoices, a bank loan isn’t a practical option because it takes too long to fund and requires banks to be in near perfect condition.

Read more: 10 Merchant Cash Advance Alternatives & How to Choose

Small Business Administration (SBA) Loans

SBA loans are issued by banks and credit unions and are partially guaranteed by the Small Business Administration. This guarantee allows lenders to offer lower rates and longer repayment terms than they’d extend on a conventional loan. Interest rates typically fall between 6% and 13%, making them genuinely attractive for businesses that qualify.

The catch is that SBA loans are even more documentation-intensive than standard bank loans. Between gathering documentation, underwriting, and the SBA’s own review process, approvals routinely take 60 to 90 days or longer. SBA 7(a) loans are the most widely used and can fund up to $5 million for working capital, equipment, or expansion. Microloans, capped at $50,000, are worth considering for smaller capital needs.

Another practical risk worth knowing is that if an underwriter finds an issue with your application 75 days into underwriting, for example, it’s possible that they may reject your application at the last minute.

Asset-Backed Loans

Asset-backed loans use your business property as collateral (e.g., vehicles, commercial real estate, equipment, or inventory). Because the lender has a claim on something tangible if you default, they can typically offer lower rates than unsecured financing options.

For plumbing businesses with valuable assets, a fleet of service vans, owned commercial property, or high-value equipment, this can be a way to access larger loan amounts at lower cost. But the tradeoff is a slower process: lenders require appraisals and documentation on the collateral, and the underwriting process often takes weeks.

However, the larger risk is that if your business hits a rough patch and you can’t repay, the lender can seize the assets you pledged. For plumbing businesses, losing a service vehicle or a key piece of equipment to a lender directly affects your ability to operate and generate the revenue you’d need to recover.

Asset-backed loans tend to be best for plumbing businesses with significant assets, a need for lower rates than unsecured products offer, and a clear-eyed understanding of what’s at stake if repayment becomes difficult.

Equipment Loans

As the name suggests, equipment financing is a loan specifically for purchasing business machinery or tools, with the asset itself acting as collateral. For plumbing businesses, this covers service vehicles, pipe threading machines, camera inspection systems, hydro-jetting units, and other high-cost tools.

Because the equipment secures the loan, lenders take on less risk and can offer competitive rates with repayment terms that often extend up to seven years.

However, the problem with equipment loans is that the funds can only be used to buy equipment. The process also involves vendor quotes, equipment appraisals, and documentation that typically takes several weeks, making it a poor fit if you need to replace a broken piece of equipment immediately.

Equipment loans are a good option for plumbing businesses that have time to plan an equipment purchase and want to finance it at a lower cost than a general cash advance without pledging other business or personal assets as collateral.

Business Lines of Credit

A business line of credit gives you access to a revolving pool of funds you can draw from as needed and repay on your own schedule. Unlike a cash advance, you only pay interest on what you’ve actually drawn, not the full credit limit.

For plumbing businesses managing ongoing cash flow gaps, a line of credit is often a better structural fit than a lump-sum advance. You draw to cover materials or payroll, repay when the invoice clears, and the credit resets for the next cycle. At Redline Capital, we offer lines of credit up to $750,000 that can close in 24 to 48 hours.

But it’s worth mentioning that qualifying for a line of credit typically requires a stronger financial profile than an MCA. Most lenders want established credit history, a solid operating track record, and some will require collateral. Credit limits may also fall short of what’s needed for major capital expenditures.

Lines of credit is best for plumbing businesses with solid credit that need flexible, repeating access to capital for ongoing cash flow management rather than a one-time lump sum.