To qualify for a traditional bank loan, ecommerce businesses need to be in near-perfect financial condition. They need excellent credit, collateral worth more than the loan amount, a long operating history, low debt-to-income, and significant cash reserves.

Because of these unrealistic requirements, an increasing number of ecommerce businesses are moving away from traditional debt and turning to revenue-based financing (RBF).

Qualifying for revenue-based financing is much easier. You can get funded in under 24 hours, and you don’t need collateral or personal guarantees.

In this article, we explore how revenue-based financing can help your ecommerce business, as well as give a breakdown of other popular ecommerce funding options.

- What is revenue-based financing?

- What are the requirements to qualify for revenue-based financing?

- How to apply for revenue-based financing

- Type of revenue-based financing options

- Why choose Redline Capital

- Alternatives to revenue-based financing

Want to know what rates and loan amounts you qualify for? Use our revenue-based financing pricer to generate instant quotes.

What Is Revenue-Based Financing and How Does It Work?

As the name indicates, revenue-based financing is a non-dilutive funding model evaluated and approved based on a business’s revenue.

This makes qualifying for revenue-based financing much easier than bank loans because lenders don’t look at your profit margins, collateral, cash reserves, and other eligibility criteria. As long as you meet the lender’s minimum monthly revenue requirement, you qualify. At Redline, that’s $30,000 per month.

This simple approval process also means revenue-based financing can be funded much faster than bank loans, typically within 24 hours. Banks evaluate countless requirements and paperwork, resulting in 60 to 90-day wait times for funds.

The third benefit of revenue-based financing is that it can fund much larger amounts than banks. Banks are extremely cautious lenders and will only lend 50% of your monthly revenue at most, while many revenue-based financing lenders can fund up to 200%.

Revenue-based financing works like this: ecommerce businesses receive a lump sum upfront, usually 150% to 200% of their monthly revenue, and pay it back as a percentage of future revenue.

Ecommerce brands often face seasonal spikes, such as Black Friday. But if sales drop during a slow month, the repayment amount decreases accordingly, preserving essential cash flow. This funding allows them to pay back more during high sales periods and less during quiet periods.

Read more: Why Use Revenue-Based Financing Instead of Debt Financing?

What Are the Requirements to Qualify for Revenue-Based Financing?

To qualify for revenue-based financing, you simply need to demonstrate to the lender that you meet the monthly revenue threshold.

For example, to qualify with Redline Capital, your ecommerce business needs to:

- Earn at least $30,000 in gross monthly revenue

- Be in practice for 12 months or more

- Be located in the U.S.

To confirm your monthly revenue history, you only need to submit four months of bank statements. This allows our team to underwrite your application quickly, and we can send you the funds on the same day you apply. Over 80% of businesses that apply to us get approved.

On the other hand, getting a loan from a traditional bank can be more challenging. They usually follow a much stricter criteria and request detailed information about your business, including:

- A strong credit score, often 720+

- At least 2 to 3 years of active trading

- High annual revenue, often exceeding $500,000

- Tangible assets as collateral, including real estate, equipment, or inventory

- Cash reserves worth three months of operating expenses

- Debt-to-income ratios under 35%

These loans are difficult for ecommerce businesses to secure because the bank’s risk assessment models are designed for brick-and-mortar companies rather than digital online businesses.

Banks generally require physical collateral as security for a loan. Most ecommerce brands lack these assets, and their value lies in digital presence, customer lists, and inventory. None of these are typically accepted as valid collateral.

In addition, banks ask for 2–3 years of tax returns and high credit scores, but they struggle to interpret ecommerce-specific KPIs that actually indicate health, such as Return on Ad Spend (ROAS) and Customer Acquisition Cost (CAC), as well as digital footprint and social media engagement.

How to Apply for Revenue-Based Financing

At Redline Capital, our application and approval process is simple and can be completed in just a few minutes:

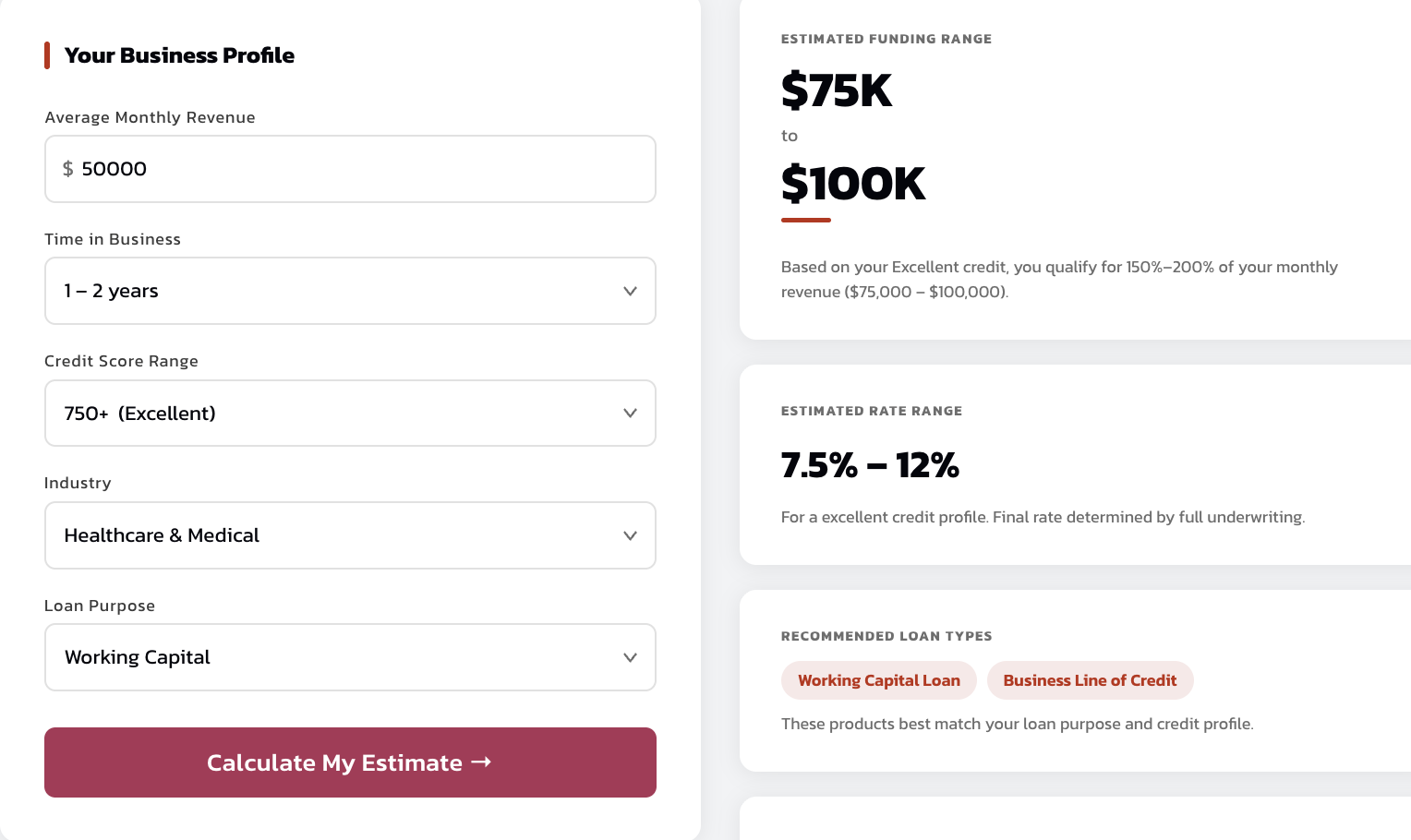

- Generate an instant quote using our loan pricer. Enter your monthly recurring revenue, time in business, credit score, industry, and loan type. The pricer will show how much you qualify for and at what rate. Here’s what that looks like.

- We’ll ask you to submit four months of bank statements. We don’t need tax returns, balance sheets, or other financial statements.

- Our underwriters run a soft credit check (which does not impact your credit score) and review your application. We won’t reject you just for having bad credit, but good credit helps you qualify for lower rates, more flexible terms, and larger sums.

- We send you multiple offers for different revenue-based financing products within a few hours. These include term loans, working capital loans, cash advances, and business lines of credit. Each offer outlines the total repayment amount, type of funding, rates, weekly or monthly payments, repayment structure, and APR.

- You choose the offer that works best for your business. No pressure from us.

- Once you accept an offer, you receive the funds in your bank account within one or two hours.

Read more: How Does Revenue-Based Financing Work?

Types of Revenue-Based Financing Options

Some of the financial products we offer ecommerce businesses include:

- Term loans are lump-sum financing options designed for online businesses to purchase inventory, launch marketing campaigns, or manage cash flow. Repayment for the borrowed amount is over a set period, typically 1 to 3 years.

- Working capital loans are short-term financing solutions designed to cover day-to-day operational costs rather than long-term investments. They help ecommerce businesses bridge cash flow gaps, buy inventory, manage seasonal demand, or respond to unexpected expenses. We offer loans up to twice your monthly revenue, typically repaid over 6 to 24 months.

- Business line of credit is a revolving credit facility that allows ecommerce sellers to withdraw funds up to a pre-approved limit. A line of credit works like a credit card: you borrow only what you need and only pay the amount actually withdrawn.

- Equipment loans are specialized financing options used to acquire the physical or digital assets needed to run an ecommerce store. At Redline Capital, we offer up to 100% financing; no personal guarantees or down payments required.

Regardless of the type of revenue-based financing, we evaluate the same thing: your monthly revenue.

Why Choose Redline Capital for Your Revenue-Based Financing

You may have settled for revenue-based financing, but the actual lender you choose still matters.

On one hand, going with a high-quality lender helps your ecommerce business secure low rates and fast access to funds. On the other, picking a predatory or unscrupulous lender may rush you into a decision that is not the best for your business.

Here are 3 reasons to pick Redline Capital over other RBF providers:

You Can Secure Lower Rates with Us

Businesses that apply through Redline Capital consistently secure lower rates than they’d find elsewhere.

Over the years, we’ve established strong relationships with premium business lenders, including OnDeck, Headway Capital, Rapid Finance, and Biz2Credit.

We’ve sent them loan applications worth hundreds of millions of dollars, helping them grow their lending business. In exchange, these lenders give our applications discounted rates, more flexible repayment schedules, and larger funding amounts that are not accessible to direct applications.

Essentially, when you apply with Redline Capital, you put all the deals we sent our lending partners to work for your business, allowing you to secure lower rates.

Redline Capital offers two additional benefits:

- We send your application to several lenders and present you with multiple offers from different lenders with just one application. This means you can compare offers from multiple lenders without having to spend the time submitting separate applications for each one.

- We have developed strong relationships with specific staff members who work at our lending partners. If your business needs emergency funds for extreme situations, we can call on them rather than going through a formal application. This allows us to achieve rapid funding times, sometimes under 4 hours.

We Have Ecommerce Financing Expertise

At Redline Capital, we understand that ecommerce businesses have unique financial characteristics, including a lack of physical assets, a heavy reliance on technology, and highly seasonal sales cycles.

Often, traditional lenders struggle to assess these businesses accurately and their sources of revenue. The problem is that ecommerce businesses’ value is tied to intangibles like digital storefronts, website traffic, customer lists, and fast-moving inventory, which many bank systems cannot assess.

In addition, ecommerce businesses often have revenue sources dispersed across multiple sales channels and accounting tools. This mix further delays an already slow underwriting process from traditional banks. As such, banks end up seeing these businesses as high risk and either reject their applications or offer loans with high interest rates.

In contrast, at Redline Capital, all we ask for is 4 months of bank statements, and you can have the funds today or tomorrow. We don’t need equity or collateral. Payments are calculated as a percentage of monthly sales, so they automatically adjust to seasonal revenue dips, which is ideal for a seasonal online business.

We Are a Professional, Ethical, Low-Pressure Lender

At Redline Capital, we always behave in a friendly but professional manner. We answer any questions you may have during your application and send you the offers you qualify for. We leave the decision entirely up to you and never pressure you to accept any offers. You can take as long as you need to review the terms, and if you decide to choose a different lender, we accept your decision.

In the event that you don’t qualify for the financing product you originally applied for, we’ll send you extra offers for alternative products for which you do qualify, along with some guidance on what to do next. We never just reject your application like traditional banks do.

If you feel that you’re being coerced into accepting an offer that may not be the best for your business, our advice is to walk away from such unscrupulous and unethical lenders. When choosing a lender, make sure you read unbiased online reviews regarding the lender you’re considering and, if possible, talk with previous clients.

Here’s what some small business owners have said about our application process:

Check out our case studies page to hear more about our borrowers’ experiences:

Secure Fast and Affordable Revenue-Based Financing with Redline Capital

Use our automated loan pricer to generate instant quotes and calculate the loan amounts and rates your business can qualify for.

Alternatives to Revenue-Based Financing

If you find that revenue-based financing is not the best option for your business, here are some alternatives that may suit what you need.

Traditional Bank Loans

Traditional bank loans remain a popular choice for established ecommerce businesses. They typically offer the most competitive interest rates and can fund large amounts for major investments like warehouse acquisition or large-scale product launches. Fixed monthly schedules provide predictability and strengthen the business credit score, facilitating better terms for future borrowing.

However, they present significant hurdles for startups and those with fluctuating sales. Due to the extensive paperwork needed, approval can take weeks or even months. These lenders often require tangible assets (like property or equipment) as collateral, which many online businesses may not have.

In addition, fixed payments don’t adjust for seasonal dips or sudden revenue drops common in ecommerce. Traditional banks also struggle to evaluate digital business with intangible assets such as brand value.

SBA Loans

SBA loans are government-backed loans that offer ecommerce businesses a balance between the low costs of traditional banking and more flexible qualification criteria.

The SBA doesn’t lend money directly; instead, it guarantees 50% to 85% of the loan, making lenders more willing to approve businesses that may have been denied by traditional banks. Interest rates are often lower than alternative lenders and are capped by the SBA, typically ranging from 5% to 11%, with terms that can extend to 25 years.

While they are highly competitive, nearly all SBA loans require a personal guarantee from anyone owning 20% or more of the business, meaning personal assets may be at risk if the business fails. Also, business owners must provide extensive records, including years of tax returns and detailed cash flow projections, and it can take up to 90 days to get approved and funded.

Invoice Factoring

Invoice factoring is a specialized financing tool primarily suited for B2B ecommerce and SaaS businesses that sell to other companies on credit terms. This form of funding involves selling unpaid invoices to a third-party “factor” for an immediate cash advance, typically 70% to 90% of the invoice value. It is generally not suitable for B2C ecommerce stores (selling directly to consumers), as these transactions do not typically generate the necessary invoices.

One of the main advantages is that businesses can access funds within 24–48 hours rather than waiting the typical 30, 60, or 90 days for customer payment. Also, because it involves the sale of an asset (the invoice) rather than a loan, it does not add debt to the business. Approval is based on your customers’ creditworthiness rather than your own business credit score, making it more accessible for startups or businesses with poor credit.

Fees typically range from 1% to 5% per invoice, which can be significantly more expensive than traditional bank loans. Also, the factor interacts directly with your customers to collect payments. This may be perceived as a sign of financial instability and can damage your professional relationships if aggressive collection tactics are used. If you have customers who frequently dispute invoices or fail to pay, you must buy back the invoice or replace it with a new one, potentially giving your business cash flow issues.

Equipment Financing

Equipment financing for ecommerce allows businesses to acquire high-cost physical assets, such as warehouse machinery, shipping automation tools, and IT infrastructure, and spread the cost over time. Because the equipment itself serves as collateral, it is generally faster and easier to qualify for than traditional loans, even for businesses with limited credit history. However, these loans don’t typically cover all the costs, and you’re expected to make a down payment of 10% to 30%.

Interest rates range between 8% to 30%, depending on your credit score and the equipment type. Repayment terms usually match the equipment’s useful life, often 2 to 7 years.

Instead of buying, some businesses opt to get funding to lease their equipment. This allows for regular upgrades, which is vital for ecommerce tech stacks (like AI servers or automated sorting) that evolve rapidly. The disadvantage is that your business doesn’t own the asset at the end of the term, meaning it builds no equity and cannot be used as collateral for future loans.

Business Credit Cards

Business credit cards serve as a flexible, high-speed financing tool for ecommerce businesses, particularly useful for managing daily operational costs and seasonal inventory spikes. The main disadvantage is that they carry some of the highest interest rates and often require personal liability from the business owner.

Approval often happens in minutes or days, providing instant funding for time-sensitive needs like a flash sale or emergency inventory restocking. However, credit limits are usually lower than what you might get with a term loan, often starting at $5,000 to $25,000 for newer businesses. Consistent, on-time payments also help establish your business credit score, which is essential for securing larger, lower-interest loans in the future.

Merchant Cash Advances

Merchant Cash Advance (MCA) is a funding solution where an MCA provider gives an upfront lump sum in exchange for a fixed percentage of future daily sales. For ecommerce businesses, this is particularly effective for managing seasonal fluctuations, as repayments automatically scale with revenue.

Qualification is based on sales performance rather than credit history or collateral. Businesses with poor or limited credit can often still secure funding as long as they show consistent card transaction volume. Approval is fast, typically within 24 to 48 hours.

MCAs generally use factor rates ranging from 1.18 to 1.49. This means you will have to pay between $118,000 and $149,000 for a cash advance of $100,000, making it one of the most expensive ways to borrow. Constant daily or weekly deductions from your sales can reduce your working capital and may strain operations if your profit margins are already tight. In addition, successfully paying off an advance will not help build your business credit history.

Platform Lending

Platform lending, such as Shopify Capital, Amazon Lending, or Stripe Capital, uses your online store’s real-time sales data to provide a form of revenue-based funding.

Since the platform already tracks your sales, there is often no paperwork or credit check; offers may even appear as a “pre-approved” notification in your dashboard. Funds are typically deposited into your account within 24–48 hours of acceptance. Platforms understand ecommerce metrics (like conversion rates and return on ad spend) better than traditional banks, making them more likely to fund online-only businesses.

The main disadvantage is that you’re restricted to using the platform’s payment gateway. Switching to a different ecommerce platform becomes difficult until the debt is cleared. The capital is often intended for growth (such as inventory and marketing), and most platforms do not allow the funds to be used to pay off other debts or purchase real estate, for example.

Peer to Peer Lending

Peer-to-peer (P2P) lending, also known as “social lending” or “P2B” (Peer-to-Business) lending, connects ecommerce businesses directly with individual investors. For online retailers, it serves as a fast funding alternative to traditional bank loans, though it often requires personal risk and can be more expensive for those with limited credit history.

P2P platforms use less strict criteria than traditional banks, making them more accessible to startups or businesses with limited trading history. By cutting out the banking middleman and overhead costs of physical branches, platforms can sometimes offer lower interest rates than traditional banks for businesses with good credit. Typically, the application process is entirely digital and can take as little as 30 minutes, with funds often available within three days to two weeks.

Many P2P loans require a personal guarantee, putting your personal assets at risk if the business fails to repay. These platforms also charge arrangement or origination fees ranging from 1% to 6% of the total loan amount.

Asset-Based Lending

Asset-Based Lending (ABL) is a strategic financing model for ecommerce businesses that use their own balance sheet (specifically inventory, accounts receivable, and equipment) as collateral to secure a revolving line of credit or a term loan. Unlike traditional loans that focus on historical cash flow, ABL prioritizes the liquidity and value of the assets themselves.

Modern digital ABL platforms use AI-driven risk evaluation to approve and fund businesses in as little as two to four weeks, significantly faster than traditional bank loans. In addition, as the loan is secured by tangible assets, it is considered lower risk for lenders than unsecured options, often resulting in more favorable rates.

However, if your inventory value drops or your receivables decrease during a slow season, your available credit line may decrease exactly when you need it most. In addition, borrowers must provide regular reports, which can be burdensome without automated systems.

Equity Financing

Equity financing is the process of raising capital by selling ownership shares to investors, such as angel investors or venture capital, in exchange for cash. Unlike debt financing, it requires no regular repayments or interest, but investors gain a stake in the company and share in its future profits.

Strategic investors often provide more than just cash. They offer mentorship, industry connections, and operational support to help refine business models and expand into new markets. Equity rounds typically unlock much larger sums than traditional business loans. For ecommerce, this can fund expensive initiatives like proprietary product development or international logistics infrastructure.

However, securing equity is time-consuming, often taking 3–6 months. It requires extensive due diligence, detailed financial forecasting, and multiple pitches, which can distract ecommerce entrepreneurs from day-to-day operations.

In addition, business owners will no longer have full ownership. Large investors may also demand a say in major business decisions and may require board seats. This can lead to conflicts regarding the company’s strategic direction or even the removal of founders from leadership roles.

While there is no immediate interest, equity is ultimately the most expensive form of capital. If the business becomes highly successful, the value of the shares given away may exceed what the interest on a loan would have been.

Conclusion

There are many different options for your ecommerce businesses to get funding. The best solution depends on the business and the purpose of the loan.

Many ecommerce businesses (especially more established ones) still rely on traditional banks, but many are starting to turn to more flexible lenders, such as revenue-based financing.

For ecommerce, traditional banks are becoming old-fashioned. These lenders haven’t developed the tools yet to understand digital businesses with fewer tangible assets and different sources of revenue. There are some situations, however, where these lenders may be the most suitable option. For major projects, such as purchasing a warehouse or heavy machinery, a longer repayment period that comes with a traditional loan is generally more suitable than the short-term nature of revenue-based financing.

In most cases, revenue-based financing is considered a superior option for ecommerce businesses, particularly those in high-growth or seasonal phases. This form of funding is preferred for its speed, flexibility, and easier qualification. This is what we offer at Redline Capital.

Fast and Easy Financing for Your Ecommerce Business

Run our automated loan pricer to get instant quotes on the loan amounts and rates available to your business.