Lawn care businesses and landscaping companies commonly use cash advances to access quick business funding for urgent expenses or to expand operations.

You get money in your account without the strict requirements of traditional lenders or the 30 to 60-day wait.

In practice, however, many cash advance providers can’t deliver same-day or next-day funding, despite what their websites claim. We’ve heard from countless entrepreneurs who were promised same-day funding, only to be delayed and miss payroll and other critical expenses.

For that reason, don’t take funding speed claims at face value. Instead, check how much paperwork is required — it’s the most reliable way to predict how quickly they can fund.

If a cash advance company asks for extensive documentation, it’s unlikely they’ll close quickly. They’ll need time to evaluate and underwrite it, which can take days or even weeks. The fastest companies keep paperwork to a minimum.

With that in mind, we review 7 cash advance providers that work with lawn care businesses and rank them based on how quickly they can close.

We start by exploring our own offering and show how we fund faster than most companies while maintaining competitive rates.

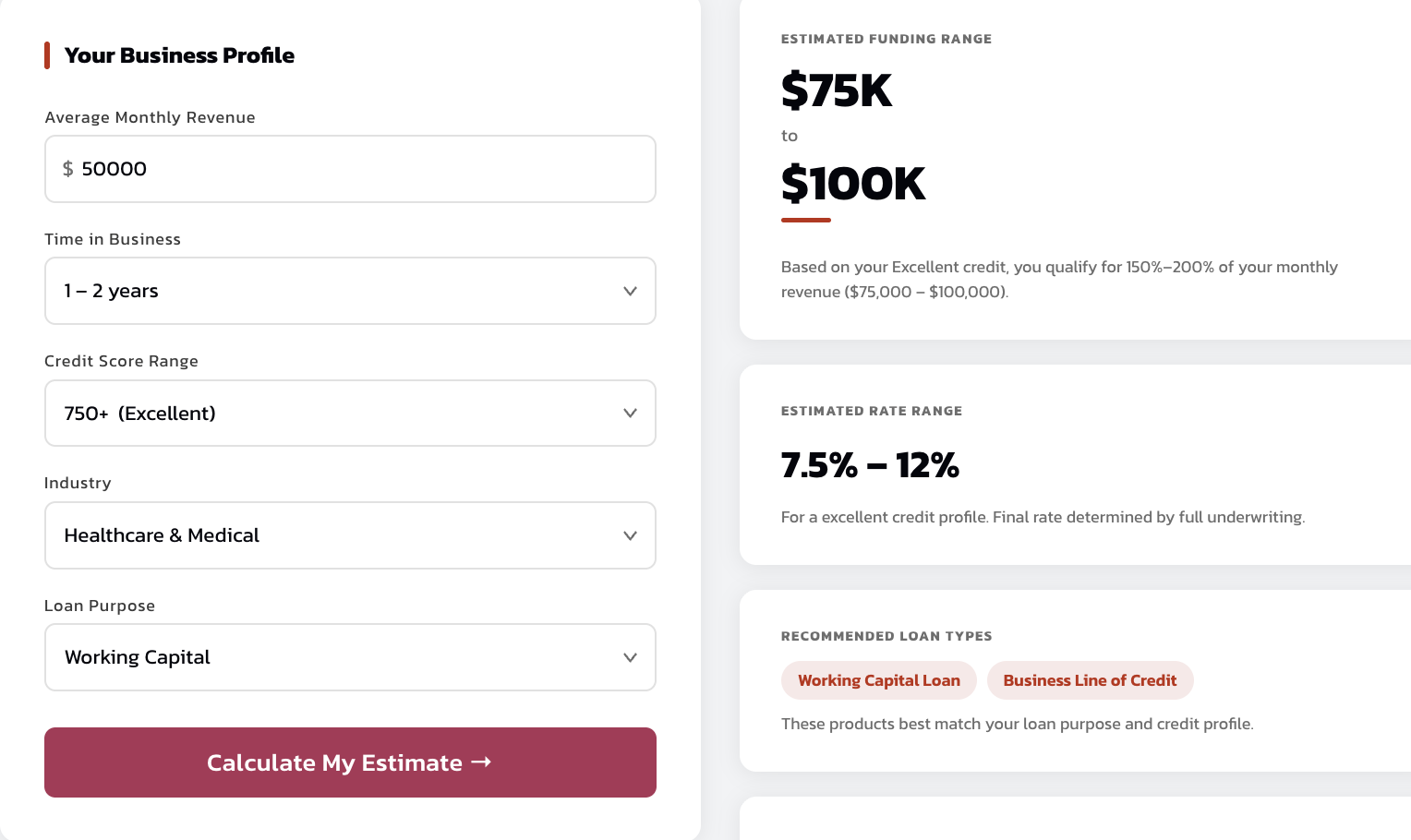

Use our business loan pricer to calculate the loan amounts and rates you qualify for.

1. Redline Capital

Qualify for a Same-Day Cash Advance with Just 4 Months of Bank Statements

At Redline Capital, merchant cash advances are based solely on your monthly revenue.

If your bank deposits show at least $30,000 per month, you can qualify for a cash advance. This simple requirement makes it easier to qualify than small business loans from banks and many other loan options. We don’t require perfect credit scores, strong profit margins, hard collateral, or deep cash reserves.

Because we evaluate your revenue rather than your entire financial profile, the only paperwork needed is four months of bank statements — allowing us to move quickly. No tax returns, credit history reviews, balance sheets, or profit-and-loss statements.

Most lawn care businesses that apply with us receive offers in their inbox within 1 to 2 hours and receive their advance the same day. In urgent situations, such as new equipment purchases or payroll, we’ve funded business owners in as little as 4 hours.

Here’s what landscaping business owners say about our cash advance options:

How to Apply for a Lawn Care Business Cash Advance with Redline Capital

Our loan application takes less than five minutes:

- Enter a few details about your business into our pricer and see how much you qualify for and the rate on your advance.

- Once you’re ready to move forward, submit four months of business bank statements. This is the only document we ask for.

- We review your revenue and run a soft credit check. A soft check has no impact on your personal credit score, and having bad credit doesn’t disqualify you.

- We send you multiple offers within a few hours. Each offer details the advance amount, factor rate, total repayment, monthly payments or weekly payment frequency, and term length.

- Choose the offer that works for your specific business needs and let us know. There’s no deadline pressure and no obligation to accept.

- Funds are wired to your business bank account the same day. From submitting your bank statements to receiving funds, the entire application process typically completes within 24 hours.

Read more: How Does Revenue-Based Financing Work?

What Sets Redline Capital Apart From Other Cash Advance Providers

We believe that fast funding should be table stakes. Here’s what else sets us apart from other financing options.

You Can Secure Lower Rates Applying with Us

Lawn care businesses typically secure lower rates when they apply with us compared to other cash advance providers.

That’s because we’re a broker with a network of premium lending partners, including OnDeck, Rapid Finance, Headway Capital, and more.

Over the past decade, we’ve delivered hundreds of millions of dollars in loan volume to these lenders. That relationship translates into tangible benefits for our clients because, in exchange for all our business, they provide preferred pricing, discounted rates, and larger advance amounts with more favorable repayment terms that aren’t available when applying directly.

Basically, when you apply with us, you leverage the volume of business we’ve sent our partners to access terms that individual applicants simply can’t secure on their own.

Redline Capital brings two more advantages to the table:

- With one application, we submit your file to multiple lenders and return competing offers for you to evaluate side by side. You don’t have to submit applications to multiple lenders to compare funding options, though we encourage you to shop around as much as possible.

- We’ve also cultivated strong working relationships with loan officers at our lending partners, so when a business is facing an emergency, we can reach out directly rather than routing through a standard application. In those cases, we’ve delivered emergency funding within 4 hours.

Read more: Why Use Revenue-Based Financing Instead of Debt Financing?

We Have Over a Decade of Experience Funding Lawn Care Companies

Lawn care businesses have financial patterns that can seem risky to lenders who don’t understand the industry — like revenue drops in winter, fast-depreciating equipment, thin margins during ramp-up, and rising payroll costs heading into spring.

Without that context, lenders often treat these patterns as red flags and charge higher interest rates.

At Redline Capital, we’ve worked with lawn care businesses for over 10 years. We understand the nuances of the industry and won’t penalize you for seasonal revenue swings, raise rates when margins compress in the off-season, or misread routine patterns as signs of instability.

This experience directly impacts both your approval odds and the rates you receive.

We Never Pressure You to Accept an Offer

Something we’ve noticed in the industry is that the more aggressively a provider pushes you to accept their offer, the worse the offer usually is. Providers that bombard you with calls and emails the moment you apply are typically trying to get you to commit before you have a chance to shop around and realize what other loan options are available.

At Redline Capital, we send you offers and step back. No follow-up pressure, no manufactured deadlines, no calls pushing you toward a decision. We encourage you to compare what we send against other providers. We’re confident that when you do, our rates and repayment terms hold up, but we’d rather have you confirm this yourself by shopping around.

Secure a Same-day Cash Advance for Your Lawn Care Business with Redline Capital

Use our automated MCA calculator to see what amounts and rates you qualify for.

2. Giggle Finance

Giggle Finance, based in Miami, is a direct MCA lender that specializes in working with small businesses, freelancers, and gig workers, making it a natural option for solo plumbers with lower revenue who don’t need large loan amounts.

They offer cash advances ranging from $1,000 to $10,000 for new borrowers, and up to $20,000 for repeat customers. There’s no business credit check, and the revenue threshold to qualify is low, making it accessible for very small or early-stage operations.

However, their cost structure is worth scrutinizing closely because they charge a factor rate between 1.15 and 1.7, then add a 7.25% origination fee on top, which is deducted from your funds before you receive them. This large origination fee puts Giggle Finance on the more expensive side compared to Redline Capital and other MCA providers.

Unlike Redline Capital, Giggle Finance is a direct lender. That means there’s no network of competing lenders behind the scenes working to offer you preferred pricing. There’s no way to know if a better deal exists without applying somewhere else separately.

3. Credibly

Credibly is a direct lender offering MCA amounts up to $600,000, with factor rates starting at 1.11 and an early repayment discount that many MCA providers don’t offer.

Beyond MCAs, they also provide access to SBA loans (Small Business Administration), business lines of credit, equipment financing, and invoice factoring, a wider product range than most MCA-only providers.

The qualification bar is higher than providers that underwrite solely on bank statements. Credibly requires a minimum credit score of 500, at least 6 months in business, and $15,000 in monthly revenue. For larger advance requests above $50,000, they request up to 6 months of bank statements. If your credit score sits below 500, you won’t qualify.

As a direct lender, Credibly can only offer you its own rates, since there’s no competing lender network driving terms down for you.

That’s worth noting because Redline Capital is a lending partner of Credibly. When you apply through Redline, we submit your file to Credibly alongside our other lending partners and return better competing offers than they can put together. Businesses applying through us consistently secure better rates than they’d get by applying directly to Credibly, because our loan volume gives us preferred pricing that individual applicants don’t have access to.

4. Biz2Credit

Biz2Credit is a lending platform offering term loans, revenue-based financing, lines of credit, and commercial real estate loans in addition to MCAs.

The product breadth is useful if you’re weighing multiple options and want financing terms that are longer-term and less expensive than regular MCAs.

Biz2Credit also funds up to $2 million across its product range, making it a good option for larger, more established lawn care businesses that have outgrown the advance limits most MCA providers cap at.

That said, Biz2Credit typically requests tax returns for the past 2 years, bank statements, a profit-and-loss statement, and credit card processing statements. That’s a documentation package closer to a bank loan than a cash advance. No matter what their turnaround time says, a provider who has to review and underwrite that volume of paperwork cannot close as quickly as one that only needs bank statements.

Like Credibly, Biz2Credit is one of Redline Capital’s lending partners. Applying through Redline means we submit your file to Biz2Credit as part of a competitive process, and you receive their best available offer alongside offers from our other partners.

The rates we return through that process are consistently better than what Biz2Credit offers individual applicants directly, because our lending volume earns preferential terms that aren’t available directly.

5. Crestmont Capital

Crestmont Capital is a direct lender offering MCAs, revenue-based financing, working capital loans, business lines of credit, and invoice financing. Their requirements sit in the middle range of MCA lenders: a 550 minimum credit score, at least six months in business, and three to six months of bank statements, depending on the advance size.

The product variety is a genuine benefit if you’re unsure which type of financing best fits your situation — their funding specialists will review your profile and recommend the most appropriate product.

That said, being a direct lender means that you can only access the public rates that they offer everyone else. You can’t leverage a broker’s loan volume to secure discounted rates and larger loan amounts. If you want to compare offers across multiple lenders, you’ll have to submit multiple applications.

Frequently Asked Questions

What are the requirements for obtaining a cash advance for my lawn care business?

Requirements vary by provider. Most MCA providers evaluate two things: how long you’ve been in business and how much revenue you generate each month. At Redline Capital, we require $30,000 in monthly deposits, 12 months in business, and four months of bank statements. No credit score minimums, tax returns, collateral, or cash reserves needed.

How much income do I need for a $500,000 business loan?

It depends heavily on the loan type. For a traditional bank loan or SBA loan, lenders typically look for a debt service coverage ratio of at least 1.25, meaning your net operating income needs to comfortably exceed your loan repayment obligations.

For an MCA, most providers advance between 100% and 200% of your monthly revenue. To qualify for $500,000 through an MCA, you’d typically need $250,000 to $500,000 in average monthly deposits.

How hard is it to get an SBA loan?

SBA loans have the most demanding eligibility requirements of any small business financing product. Lenders typically want a personal credit score of 680 or higher, at least two years of operating history, collateral, and a full documentation package including tax returns, financial statements, and a business plan. The approval process commonly takes two to four months, sometimes longer.

Can I get a grant to start a lawn care business?

Grants exist, but they’re rarely a reliable primary funding source for a lawn care startup. Federal programs like the USDA offer grants tied to agricultural and rural development, which some lawn care businesses may qualify for depending on their focus and location.

How can a line of credit help manage cash flow?

A line of credit gives you access to a pre-approved pool of funds you can draw from as needed and repay on your own schedule. Unlike a cash advance, which gives you a lump sum and starts repayment immediately, a line of credit lets you pull only what you need, when you need it, and only pay interest on the amount drawn.

Which loan is right for your lawn care business?

It depends on three things: how quickly you need the money, how strong your financial profile is, and what you’re using the funds for.

If you need capital within days and can’t meet bank eligibility requirements, an MCA is the most accessible and fastest option.

If you need ongoing access to capital for recurring cash flow gaps, a line of credit is usually more cost-efficient because you only pay interest on what you withdraw.

If you’re purchasing specific equipment, equipment financing lets you spread the cost without pledging personal assets.

How can you use landscaping business loans?

There are generally no restrictions on how you use funds from an MCA or working capital loan. Common uses for landscaping businesses include purchasing or replacing equipment like mowers, trimmers, and trailers or covering payroll during a slow collections period or off-season.