Merchant cash advances (MCAs) fund faster and are easier to qualify for than traditional loans from banks. However, the tradeoff is cost, since MCAs tend to carry higher rates and fees and shorter repayment terms.

So, we put this guide together to help insurance agencies find MCA lenders that solve both sides of that equation: fast funding without the strict qualification requirements, and rates that are reasonable.

But first, let’s cover what to look for in an MCA lender before getting to our top picks. Knowing what to prioritize can save your insurance agency thousands in unnecessary costs.

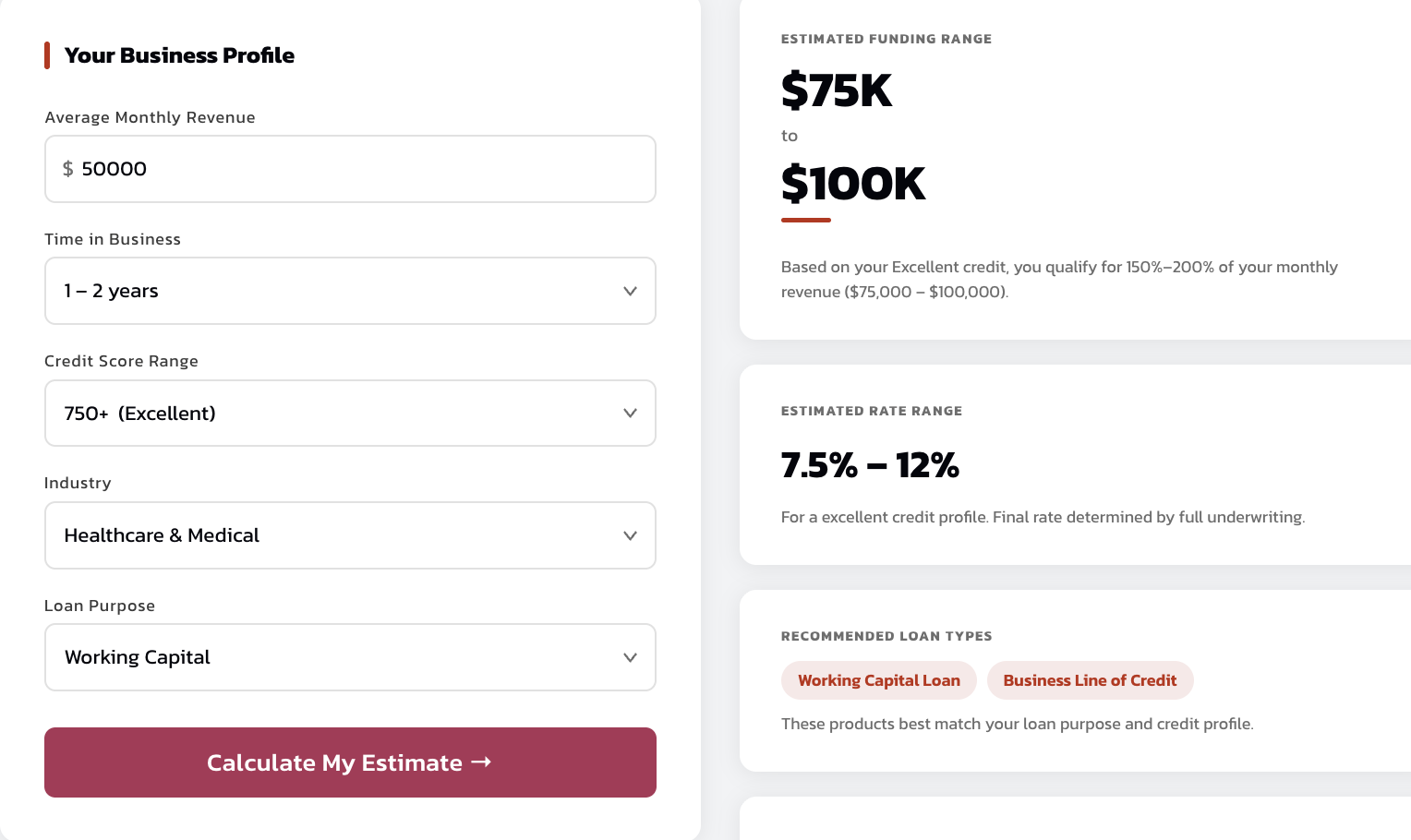

Use our MCA calculator to pull instant quotes and find out what amounts, terms, and rates your insurance agency qualifies for.

4 Factors to Consider When Choosing a Merchant Cash Advance

Are They a Broker or a Direct Lender?

Most small business owners assume that going directly to a lender is the best way to keep costs down. On the surface, that logic makes sense because if you cut out middlemen, you avoid fees they might add on top.

However, the opposite is true when you’re working with a high-quality broker.

The best brokers have spent decades sending significant loan volume to their lending partners. That volume drives a meaningful portion of a lender’s business. In exchange, they offer those brokers preferred pricing, exclusive APRs, and larger advance amountsthat aren’t available to individual applicants.

When you work with a high-quality broker, you’re essentially leveraging all the business they’ve sent their lending partners to access terms that no individual applicant could secure on their own.

How Hard Do They Push After Sending an Offer?

This is one of the most reliable ways to gauge the quality of an offer before you’ve even had a chance to compare it to anything else.

Lenders with genuinely competitive interest rates send their offer and give you room to evaluate it. They’re not worried about you shopping around because they know what they put in front of you will hold up under comparison.

Lenders with expensive offers do the opposite. They follow up repeatedly and manufacture urgency with deadlines that don’t actually exist. For instance, they may say that the offer is about to expire before the end of the day or that another business is about to take your funds. The goal is to get a commitment before you realize something better is available.

How Clear and Upfront Is Their Offer?

Many low-quality MCA lenders send offers wrapped in complex language and fine print, hoping to hide the true cost and make comparison difficult. The lack of clear disclosures on factor rates, APRs, and fees is one of the biggest problems in the MCA industry.

It’s also common for predatory MCA lenders to attract small business owners with low factor rates but build in very short repayment windows. A low factor rate spread over a short-term period has a higher APR and can put serious strain on your cash flow and profitability.

A good MCA offer lays out every number clearly before you sign, including the factor rate, APR, total repayment amount, repayment term, and any fees deducted upfront.

How Much Paperwork Do They Require?

Most MCA lenders claim on their websites that they can fund on the same day or the next day, but then they take 3 to 7 days. This is still significantly faster than traditional loans and SBA loans, but it’s impractical for insurance agents who may need to cover business needs like payroll or rent before the end of the day.

That delay is due to all the paperwork they ask for and must evaluate. Lenders who need tax returns, balance sheets, profit-and-loss statements, and credit card sales records have to review and underwrite all of it before approving your application. The fastest MCA lenders ask for very little paperwork.

Therefore, we recommend asking what documents they need upfront. The answer tells you more about their actual closing speed than any claim on their homepage.

1. Redline Capital

Same-Day Cash Advances for Insurance Agencies

Redline Capital has funded hundreds of millions of dollars in merchant cash advances for small business owners and mid-sized businesses across the U.S.

We qualify insurance agencies based entirely on monthly revenue. If your agency brings in $30,000 or more per month in revenue, you qualify.

Here is what that means in practice:

- Simple approval. Insurance agencies turned away by banks for bad credit, collateral, or documentation shortfalls qualify with us regularly. We approve 80% of applications, compared to the 13% approval rate banks extend to small business owners.

- More capital than you’d expect. We don’t cap loan amounts based on collateral or reserves. We typically advance between 100% and 200% of monthly revenue as a lump sum, while banks rarely offer more than 50% through their standard loan program.

- No personal liability. Your personal and business assets aren’t at risk. Unlike traditional loans or working capital loans that require collateral, our advances are secured against future sales only.

Here’s what insurance carriers say about our closing speed and the quality of our offers.

Here’s how we tackle the four factors outlined above.

Factor #1: We Are a High-Quality Broker With Access to Exclusive Rates

Over the past decade, we’ve sent hundreds of millions of dollars in loan volume to our lender network including Rapid Finance, OnDeck, and Headway Capital.

That volume is valuable to them because it’s a meaningful source of their business financing revenue. In exchange, they give our applicants preferred pricing, exclusive APRs, and larger advance amounts that direct applicants simply don’t receive.

We put this to the test often. We ask small business owners to send us the offer they got from one of our funding partners, and when we compare it to the quote we received, ours comes in at a lower rate nearly every time.

In addition to lower interest rates, our lender relationships give you three things a direct lender can’t match:

- One application, multiple competing offers. We submit your file to several lenders simultaneously and bring back their best offers side by side. You get a full market picture of available financing options without filling out several applications.

- Direct access in urgent situations. When an insurance agency needs working capital immediately, we call loan officers we know personally rather than routing through a standard queue. That direct access is how we’ve got businesses funded in under four hours.

- A path forward when your file is borderline. If your application falls just short of a lender’s standard criteria, we work with our partners to find a structure that gets you approved. A direct applicant in the same position typically just gets a rejection with no alternative small business financing options offered.

Read more: Business Loan Denied? Here’s How to Get Funded Same-Day

Factor #2: We Never Pressure You to Accept Our Offers

We email you offers and step back entirely. We won’t call you non-stop or pressure you to accept like many other MCA lenders do to small business owners.

We encourage insurance agencies to shop around and compare what we send against whatever else they can find. That’s because we’re confident in the quality of our offers and most businesses come back to us after shopping around.

We’d rather have you verify the quality of our business funding for yourself than manufacture urgency.

Factor #3: We Are Fully Transparent About the Cost of Every Offer

Every offer we send lays out the full picture with clear disclosures: factor rate, total repayment amount, APR, repayment term, monthly payments, and any fees deducted before funding. Nothing is buried or left for you to calculate yourself. We believe insurance agents deserve the same level of transparency they extend to their own clients when explaining policy terms.

Read more: How Does Revenue-Based Financing Work?

Factor #4: We Only Need Four Months of Bank Statements and Fund within 24 Hours

Qualifying comes down to one number: $30,000 in monthly revenue. Clear that threshold and you’re approved. We verify that from four months of bank statements, which takes us an hour or two to review. Most insurance agencies have a lump sum in their account the same day they apply. For genuine emergencies, we’ve closed advances in under four hours.

This makes us one of the fastest working capital loans available to insurance agencies, without the paperwork burden of traditional loans or SBA loans.

Here is how the full process works:

- Start with our MCA calculator. Enter your monthly revenue, time in business, and a few basic details to get an estimated advance amount and interest rates before committing to anything.

- Send us four months of business bank statements. That’s the only document we ask for.

- We check your deposits and run a soft credit pull. Your credit score doesn’t determine whether you qualify. We use it only to help set your rates and terms.

- Competing offers arrive in your inbox within the hour. Each one shows the advance amount, factor rate, total repayment, APR, monthly payments, payment frequency, and loan term so you know exactly what you’re agreeing to.

- Take as long as you need. No deadlines, no follow-up pressure. Compare what we send against anything else you find.

- Funds hit your account the same day. Once you choose an offer, we wire the lump sum directly to your business bank account within hours.

Secure Fast and Competitive Funding Options with Redline Capital

Enter a few details about your insurance agency into our automated MCA calculator to see what you qualify for.

2. Credibly

Credibly has built a strong reputation as a direct MCA lender for small business owners across a range of industries, including insurance agents and agency operators. Their merchant cash advances go up to $600,000 and factor rates start as low as 1.11, making them a good choice for insurance agencies looking for larger loan amounts at lower interest rates.

They also offer term loans and a business line of credit for agencies whose business needs go beyond a short-term advance.

Credibly can evaluate applications within one business day and fund in as little as 24 hours. We like that their documentation requirements are leaner than most traditional loans, asking only for a government-issued photo ID, three months of bank statements, and a signed receivables purchase agreement. Reviewers also consistently cite a professional and transparent experience throughout the application process.

That said, the additional documentation beyond bank statements does add some friction compared to Redline’s single requirement, which can slow things down for insurance agencies that need emergency working capital.

As a direct lender, Credibly can only quote their own interest rates. It’s also worth noting that Credibly is one of Redline Capital’s lending partners. Insurance agencies that apply through Redline receive Credibly’s offers as part of a multi-lender competitive process, and the rates we return are typically better than what Credibly offers individual applicants directly.

3. Fora Financial

Fora Financial has originated more than $5 billion in small business financing since its founding and brings considerable experience to the lending space.

Their revenue advance product offers up to $1.5 million with repayment terms as long as 18 months, giving insurance agencies access to larger loan amounts and longer repayment terms than most short-term lenders offer.

They also offer an early repayment discount, which can help insurance agents save thousands if they plan on repaying their advance early. A minimum personal credit score of 500 and monthly revenue of $20,000 make them accessible to a wide range of startup and established agency operators, including those with bad credit.

The application process starts with a quick online form followed by a call with a loan officer, with final approval typically arriving within four hours and funding within 24 to 72 hours. Some applicants may also need to provide three months of credit card sales and debit card processing statements on top of bank statements, which adds a step compared to lenders who rely solely on bank statements.

As a direct lender, Fora Financial can only offer their own interest rates. Their cost structure is worth scrutinizing before committing: factor rates range from 1.13 to 1.50, and a mandatory origination fee of at least 3% is deducted upfront from your funding amount, which reduces the lump sum you actually receive.

Some borrowers have also noted that final offers came in lower than initial discussions suggested, so it’s worth getting all details and disclosures confirmed in writing before proceeding.

4. Greenbox Capital

Greenbox Capital is a Miami-based direct MCA lender with a low barrier to entry, making them a practical option for small business owners and startup insurance agencies that need fast working capital without meeting the stricter requirements of larger lenders.

Their minimum monthly revenue requirement is $7,500, among the lowest in the industry, and they work with businesses that have bad credit or less-than-perfect personal credit scores.

Their merchant cash advances range from $3,000 to $500,000 with factor rates starting at 1.1 and same-day approvals available, with funding typically arriving within 24 hours. Reviews from small business owners are largely positive, highlighting the professionalism of their funding advisors and the speed of the funding process.

There are a few limitations worth noting. Greenbox does not publish disclosures on factor rates or APR information publicly before an application is submitted, which makes it harder for insurance agents to compare the true cost against other financing options without first going through the application process.

Some reviews also mention frequent follow-up calls after an application is submitted, which is worth keeping in mind when evaluating their offer quality.

As a direct lender, Greenbox can only offer their own interest rates with no external lending network giving you access to exclusive pricing. For insurance agencies who want to see competing offers from multiple lenders before deciding, applying through a broker like Redline Capital alongside Greenbox is a practical way to benchmark the difference in rates.

5. Rapid Finance

Rapid Finance is a Maryland-based lender that has funded over $4 billion to small business owners since its founding. The standout value of Rapid Finance is that they charge no origination or documentation fees on their MCA product, which keeps the total payback amount lower compared to lenders who deduct upfront fees before sending funds.

This makes their effective cost of working capital more competitive than their factor rates alone might suggest.

Their eligibility bar is also relatively accessible for startup and established insurance agencies, requiring a minimum personal credit score of 550, three months in business, and $5,000 in monthly revenue. Advance amounts range from $5,000 to $500,000 with estimated repayment terms of three to eighteen months, and funding can arrive within hours of approval in straightforward cases.

Their application process does require credit card sales and debit card processing statements on top of bank statements, which adds an underwriting step that can slow things down for insurance agents who need a lump sum urgently.

One thing to keep in mind: Rapid Finance operates as a direct lender, which means their interest rates reflect what they can offer independently with no external lending network driving terms in your favor.

It’s also worth noting that Rapid Finance is one of Redline Capital’s lending partners. Insurance agencies that apply through Redline receive exclusive offers due to all the small business financing volume we’ve sent Rapid Finance over the years. The rates we return are consistently better than what direct applicants receive through Rapid Finance’s own channels.