It’s common for auto repair businesses to use merchant cash advances (MCAs) to settle urgent operational expenses because they fund quickly, typically within a couple of days.

A 30- to 90-day bank funding timeline simply doesn’t work when you need to cover payroll EOD or repair a vehicle lift in the middle of a job.

However, MCAs aren’t perfect financing solutions. The MCA industry operates under significantly less regulatory oversight than traditional banking, allowing unethical lenders to charge predatory rates with little oversight.

That’s why choosing the right MCA lender matters. It can be the difference between affordable financing with flexible terms and getting trapped in a predatory deal.

We created this guide to help auto repair businesses secure fast MCAs while keeping borrowing costs low.

We start by discussing the factors that separate high-quality MCA lenders from unethical ones. We then cover how we at Redline Capital help auto repair shops secure same-day funding at the lowest possible rates.

Use our MCA calculator to generate instant quotes and see what your auto repair shop qualifies for.

How to Tell the Quality of a Merchant Cash Advance Lender

Are They a Broker or a Direct Lender?

Most auto repair businesses assume that applying directly to an MCA lender is the cheapest path, since cutting out brokers should mean fewer fees. This is true for low-quality brokers with a short track record, but the best and most experienced MCA brokers consistently deliver better rates.

That’s because high-quality brokers have sent consistent, high volumes of applications to their lending partners over many years. Lenders reward all that business with wholesale pricing, preferred APRs, and discounts that applicants don’t get when applying directly.

Put simply, applying through the right broker means your application is backed by every deal that broker has previously sent to the lender.

How Much Pressure Do They Put on You After Sending an Offer?

Watch how an MCA lender behaves after sending an offer, since it tells you a lot about its quality.

Lenders with competitive rates send their offer and give you time to evaluate it. They are confident their terms will hold up when you compare them to other lenders’ offers.

Lenders with expensive or predatory offers don’t want you shopping the market. So, they hound you with phone calls, manufacture fake deadlines, and sometimes claim another shop is about to take your funding.

The harder a lender pushes for your signature, the more likely there’s something better out there.

How Transparent Are Their Offers?

A trustworthy offer lays out the full cost of borrowing before you commit: the factor rate, APR, total repayment amount, repayment term, prepayment penalties, and any fees taken out before funds reach your account.

Some lenders intentionally make their offers confusing so it’s harder to understand the true cost of borrowing and compare them against competitors. This is another sign of a low-quality or sometimes predatory lender.

How Much Paperwork Do They Require?

A big problem we see with many MCA lenders is that they ask for way too much paperwork, and reviewing it all delays funding. In fact, we hear from businesses all the time about how lenders promised to close the next day, but then ended up taking a week or more.

That’s why we recommend considering the amount of documentation an MCA lender asks for. It’s a reliable indicator of how fast they’ll actually fund.

Lenders working through tax returns, balance sheets, accounts receivable reports, collateral, and credit card processing records are rarely able to fund same-day or next-day. The ones that consistently deliver fast funding keep their requirements short.

5 Merchant Cash Advance Lenders Compared

1. Redline Capital: Same-Day Cash Advances for Auto Repair Shops

Redline Capital is an MCA broker that has closed hundreds of millions of dollars in advances for businesses across the U.S., including auto repair businesses, body shops, and more.

Our main requirement is $30,000 per month in revenue. If your auto repair shop meets that, you qualify. You don’t have to worry about credit scores, cash flow, cash reserves, business plans, collateral, or personal guarantees like with banks.

Our accessible qualification criteria mean that over 80% of businesses that apply end up qualifying.

There are no restrictions on how you can use the advance. You can use it for equipment financing, ongoing working capital, payroll, rent, and anything else you need.

Here’s what auto repair shop owners say about working with us:

Factor 1: You Secure Lower Rates When You Apply With Us

Over the past decade, we’ve directed hundreds of millions of dollars in loan applications to our lending partners, including Rapid Finance, OnDeck, and Headway Capital.

That consistent volume is commercially significant to them, and they reciprocate with wholesale pricing, preferred APRs, and advance amounts that auto repair shops applying directly simply won’t receive.

We verify this with real data. When a shop owner brings us an offer they received directly from one of our partners, we show them what we pulled. Ours comes back with lower rates and more flexible terms nearly every time.

Our relationships with lenders also give auto repair shops two things no direct lender can offer:

- One application, multiple offers. We submit your file to several lenders at once and return competing offers side by side. You see what the full market will offer without filling out separate applications for each provider.

- Emergency access when it counts. When a shop needs capital the same day to cover an urgent expense, we contact loan officers we know personally rather than routing through a standard queue. That direct access is how we’ve funded businesses in under four hours.

Factor 2: We Never Pressure You to Accept Our Offers

Once we send an offer, we go quiet. No follow-up calls, invented deadlines, or pressure of any kind.

We can operate this way because we know our offers hold up under comparison. Most businesses that shop the market end up coming back to us.

Factor 3: Our Offers Are Fully Transparent

Every offer we send shows the complete picture before you commit: the advance amount, factor rate, APR, total repayment amount, repayment term, payment frequency, and any fees. Nothing is buried in fine print or left for you to calculate on your own.

Factor 4: We Only Need Four Months of Bank Statements and Can Close Same-day

We qualify auto repair shops on one number: $30,000 in monthly revenue.

As a result, the only document we need is four months of bank statements. We verify your revenue in under an hour, and most shops have a lump sum in their account the same day they apply.

Here is how the process works:

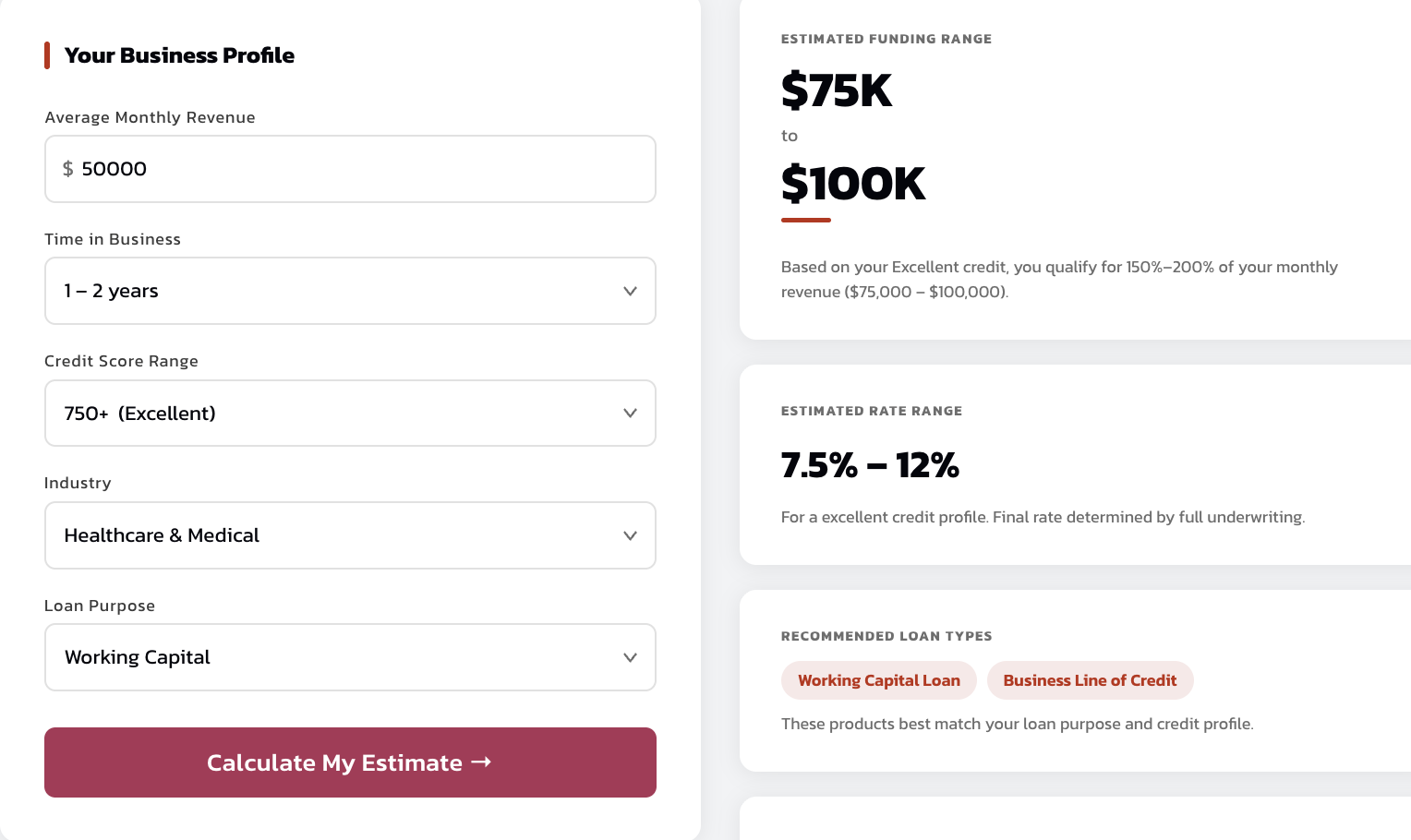

- Open our MCA calculator. Enter your monthly revenue, time in business, credit score, industry, and loan purpose to get an estimated advance amount and rate before committing to anything.

- Send four months of business bank statements. That is the only document we need.

- We check your deposits and run a soft credit pull. Your credit score doesn’t affect whether you qualify. We use it only to determine the rates and terms on your offers.

- Offers arrive in your inbox within the hour. Each one shows the advance amount, factor rate, total repayment, APR, payment frequency, and loan term in full.

- Review at your own pace. No deadlines or follow-up pressure. We recommend comparing everything we send against other auto repair shop loans before committing.

- Funds reach your account the same day. Select an offer, and we wire the advance to your business bank account within hours.

Secure Affordable Auto Repair Shop Financing with Redline Capital

Use our automated cash advance pricer to see what amounts, rates, and terms your auto repair shop qualifies for.

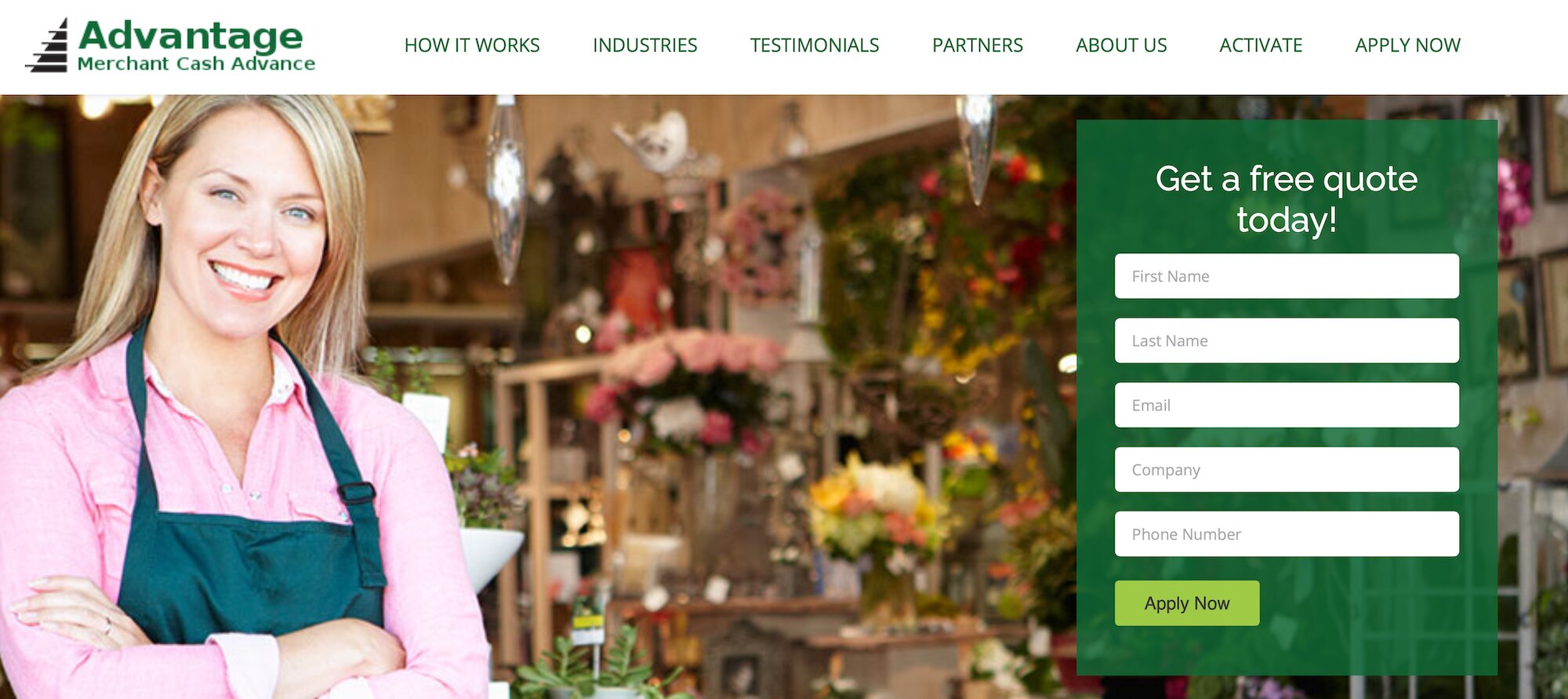

2. Advantage MCA: Best for Auto Repair Shops with Bad Credit

Advantage MCA has built their entire auto repair business lending operation around automotive businesses, giving them a level of industry-specific knowledge that most general MCA providers can’t match.

Their underwriting team is familiar with the seasonal slowdowns, insurance payment delays, diagnostic equipment costs, and payroll pressures that define the auto repair business. This means they evaluate applications with context that a generic online lender would miss entirely.

There’s no collateral required, documentation requirements are kept to a minimum, and shop owners with poor credit histories are regularly approved. Most auto repair businesses receive fast capital within 3 to 5 business days, which is still significantly faster than any bank loan or SBA loan process.

Advantage doesn’t publish a specific monthly revenue threshold publicly, so the exact eligibility criteria require a direct conversation with their team.

However, Advantage doesn’t have an automated MCA pricer like Redline Capital, where you can instantly see what you qualify for. Instead, you have to reach out to their team and enter the sales process first, which delays funding. For businesses operating on tight timelines, Redline is often a stronger fit for same-day or next-day funding.

Read more: 10 Merchant Cash Advance Alternatives & How to Choose

3. Rapid Finance: Best for Low Eligibility Requirements

Rapid Finance is a Maryland-based lender whose most compelling attribute for smaller auto repair shop businesses is how little it takes to qualify.

Their minimum monthly revenue requirement sits at just $5,000, and they’ll work with shops that have been operating for as little as three months. This makes them one of the few MCA providers genuinely accessible to newer operations with limited operating history.

Working capital loan amounts run from $5,000 to $500,000 with estimated repayment windows of three to eighteen months, giving auto repair shops flexibility across a range of cash flow and small business funding needs. Unlike many online lenders, Rapid Finance doesn’t deduct origination or documentation fees before sending funds, which means the amount that lands in your account matches the offer on paper.

However, Rapid Finance requires credit card processing records and other documents in addition to bank statements, which extends the review process compared to lenders who work from bank statements alone.

Rapid Finance is one of Redline Capital’s lending partners. When auto repair businesses come to us, we can use our relationships with loan officers at Rapid Finance to speed up the process and get you funded faster, often on the same day.

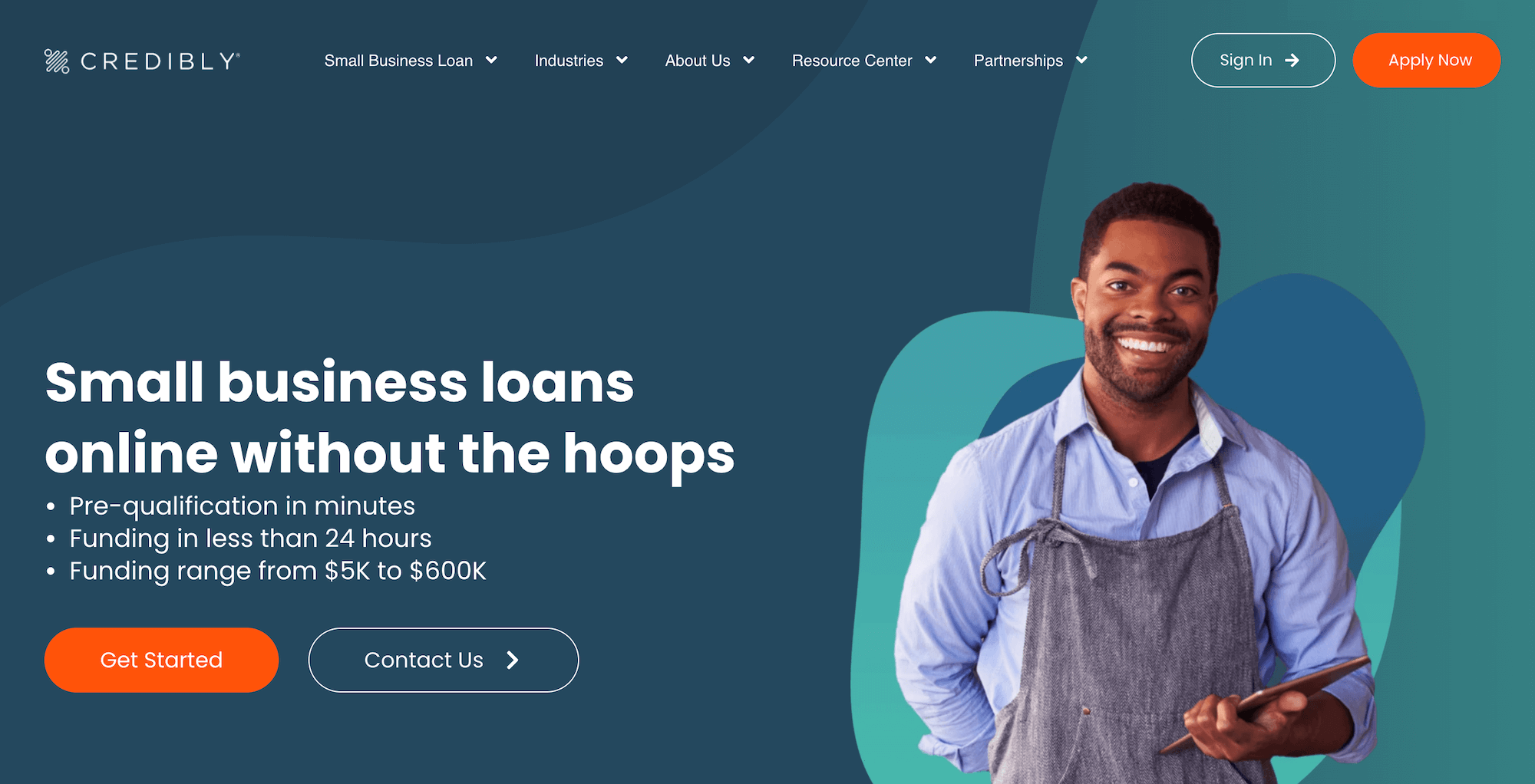

4. Credibly: Best for Larger Advance Amounts

For auto repair shop businesses that have been operating long enough to show consistent revenue and need a meaningful amount of working capital, Credibly is worth a close look.

Their cash advances reach up to $600,000, which is larger than most MCA lenders, and their starting factor rate of 1.11 sits toward the lower end of the market. We also like that they come back with decisions quickly, often within one business day.

Their documentation requirements are leaner than most bank loan applications. You simply need a government-issued ID, three months of bank statements, and a signed purchase agreement to qualify. Borrower feedback across review platforms paints a consistent picture of a professional, low-friction process.

Credibly also offers working capital loans, business lines of credit, and equipment financing alongside their MCA product, giving auto repair shops additional auto repair shop financing options if their business needs extend beyond a standard short-term loan.

But it’s worth noting that Credibly is one of Redline Capital’s lending partners, which means auto repair businesses applying through us receive more favorable rates than what Credibly offers applicants who approach them directly.

5. Headway Capital: Best for Flexible Revolving Access to Capital

Headway Capital offers a single product: a revolving business line of credit designed for small businesses that need ongoing access to working capital rather than a one-time lump sum.

For auto repair shops managing unpredictable expenses like diagnostic equipment failures, parts shortages, or payroll gaps between large insurance payments, the structure has significant advantages over a traditional auto repair business loan.

You draw only what you need at any given moment and pay interest solely on the outstanding balance rather than the full credit limit. The credit line resets as you repay, giving you ongoing access to capital without having to reapply. Headway also reports payment activity to commercial credit bureaus, allowing you to build your shop’s credit history over time.

To be eligible, auto repair businesses need a minimum personal credit score of 625, at least one year of operating history, and $50,000 in annual revenue. Unlike SBA loans or traditional bank loan products, there’s no collateral requirement.

Headway Capital is also one of Redline Capital’s lending partners. Auto repair businesses that apply through us receive more favorable offers from Headway compared to if they applied on their own.