There are many different revenue-based financing companies that all look the same on the surface, which can make it hard to find the best match for your company.

But, choosing the right one will impact the terms of the deal you end up getting (i.e., fees, payment amounts, amount of funding).

In this article, we discuss six questions to consider when choosing a revenue-based financing company for your business, including what type of provider they are, the credibility of the company, what type of businesses they support, eligibility criteria, funding amounts, and repayment terms. Then, we compare 7 revenue-based financing companies across the US, starting with an in-depth look at Redline Capital.

6 Factors to Consider When Choosing a Revenue-Based Financing (RBF) Company

1. Is the RBF provider the direct lender or a broker?

Businesses can work directly with lenders who offer RBF, or they can work with a broker. Working with a reputable broker comes with several advantages:

- Better terms — Reputable brokers can typically secure better terms than what you’d get by shopping around on your own. This is because they can rely on the relationships they’ve built with various lenders and know which ones are most likely to give a company like yours the best deals.

- Less paperwork — With brokers, you only fill out one application to see options from multiple lenders. On your own, you’d have to fill out multiple lengthy applications to compare terms. Plus, many lenders will require more financial documentation and business information than brokers, so each application process will be longer.

- Faster funding — Not only would you have to research and fill out applications for each lender you want to compare, but lenders are also typically slow to respond to individual businesses. A broker can often get a faster response because they know the right person to call, and the lender is motivated to work quickly for the broker because of their history bringing in qualified business. Working with a broker can mean the difference between securing funding in hours rather than days.

2. How Trustworthy Is the Company?

Some companies will get your information before aggressively and repeatedly contacting you until they secure a deal, even if it’s not the best option for your business. Reputable firms will use a more passive approach and just give you the information you need, answer your questions, and let you make your decision.

Additionally, the lenders the RBF provider works with can further prove their credibility. For example, OnDeck, Rapid Finance, and Headway Capital have strict vetting processes and only work with experienced and reliable RBF brokers. So, if a broker works with them, you’re likely in good hands.

3. What Type of Businesses Do They Fund?

Some RBF companies will only work with businesses in specific industries (e.g., SaaS, E-commerce), while others are open to a broader variety, such as retail, restaurants, construction, and healthcare.

Choosing an RBF company with experience helping companies in your industry will help you secure better deals. These brokers have already taken care of this for you by building established relationships with multiple lenders known for offering solid financing solutions for businesses similar to yours.

4. Is My Business Eligible for Revenue-based Funding?

Revenue-based financing often relies on a business’s ability to generate and maintain consistent revenue streams rather than traditional credit checks and lengthy financial records. However, RBF companies still assess a business’s financial health by looking at factors such as:

- Recurring Revenue: A minimum monthly recurring revenue is usually required, but the exact requirements vary from company to company. Additionally, businesses don’t necessarily have to meet the requirements every month. Oftentimes, you’ll still qualify if your average monthly revenue meets the minimum required.

- Credit Score: Most revenue-based financing companies will consider your credit score; however, a low credit score doesn’t necessarily mean you won’t qualify. Often, the credit score is just used to determine the terms of your deal.

- Financial history: Some lenders require businesses to have a proven track record of trading for at least 6 months, sometimes more.

- Debt: Some lenders prefer businesses with limited or no debt.

If you’re shopping around on your own, you may not realize you don’t qualify until after you’ve filled out the application. Brokers can help ensure that you qualify for RBF.

5. How Much Funding Can My Business Receive?

How much capital you can get will depend on the criteria discussed above. But each company will also have limits for how much they’re willing to offer any company. For example, most RBF companies will provide funding up to two times your monthly recurring revenue (MRR).

Individual lenders might also have max amounts they can offer, regardless of how much revenue you’re bringing. By working with a broker, you’re typically able to secure more funding.

6. What Are the Repayment Terms?

Payments are a fixed amount based on the last few months of your revenue, the factor rate, and the repayment period.

The factor rate indicates the total amount your business needs to pay back. Depending on your business’s financial situation, the RBF company decides on a multiple of the original investment, usually 1.2x to 1.4x the original amount.

In practical terms, this means you’ll pay $0.20 to $0.40 for every $1 of funding received. For example, if you borrow $100k at a 1.3 factor rate, you’ll pay $130k. This amount is fixed and does not accrue interest over time.

Repayment periods typically range from 6 to 18 months, but some RBF companies offer up to 24 months. Your terms will depend on various factors, including what lenders are offering at the time, your revenue, and any of the eligibility criteria mentioned above.

You’ll need to fill out an application to determine your factor rate and repayment period. Again, working with a reputable broker will make it easier and faster to shop around and ensure you’re getting the best deals.

Next, we’ll cover in detail how Redline Capital addresses each of the factors mentioned above.

1. Redline Capital: Fast Approvals, Flexible Funding & Supportive Team

Redline Capital is dedicated to your business’s success and respects the time it takes to run it. That’s why we’ll send you the best deals we find, stay available for any questions (our team’s known for quick, thorough responses), and leave the decision up to you..

With over 15 years of helping companies find the right financing option, we’ve built relationships with many reputable lenders, such as onDeck, Rapid Finance, Credibly, Biz2Credit, and Headway Capital, so we can find you some of the best deals in the industry.

Below, we’ll get into the details of who we serve, our application process, payment terms, and share what some of our customers have to say.

Competitive Options for Construction, Healthcare, Manufacturing, and More

Redline Capital can help companies in many different industries, including:

- Construction and contracting

- Healthcare

- Restaurants

- E-commerce and retail

- Manufacturing

- Professional services (e.g., legal firms, consultants)

We offer competitive deals to cover various needs, including paying for leases, purchasing stock or new equipment, covering payroll gaps, funding a marketing campaign, bidding on a new job, or fueling growth initiatives. The money can also be used as a bridge between funding rounds or for working capital needs.

Simple and Quick Application Process with Access to Multiple Lenders

Our application is quick and straightforward. All we need is for you to fill out a half-page application with details such as how much funding you need, when you need it, what you’ll use the funds for, etc. You’ll also have to provide four months of bank statements showing your monthly revenue.

We’ll review your application, run a soft credit check (so it won’t have any impact on your credit score), and come back with offers from multiple lenders in just a few hours. Every offer will outline the approved amount, factor rate, and repayment terms.

To qualify, we ask that companies:

- Have $30k recurring monthly revenue

- Be in business for at least one year

- Be located in the United States

For particularly time-sensitive needs, we can often fast-track your application process without impacting the terms of your deal. This is thanks to the relationships we’ve built with lenders over the years. Oftentimes, we’re able to secure the funding in a matter of hours because we know the right person to call, and they know us.

Flexible Deals Based on Your Needs

Redline Capital is able to offer some of the most competitive rates in the industry, starting at 1.1x, with other companies starting at 1.29x.

Funding amounts start at .5x of your recurring revenue and go up to 2x, depending on what you qualify for.

Payments can be made daily, weekly, or monthly, depending on the revenue structure of your business.

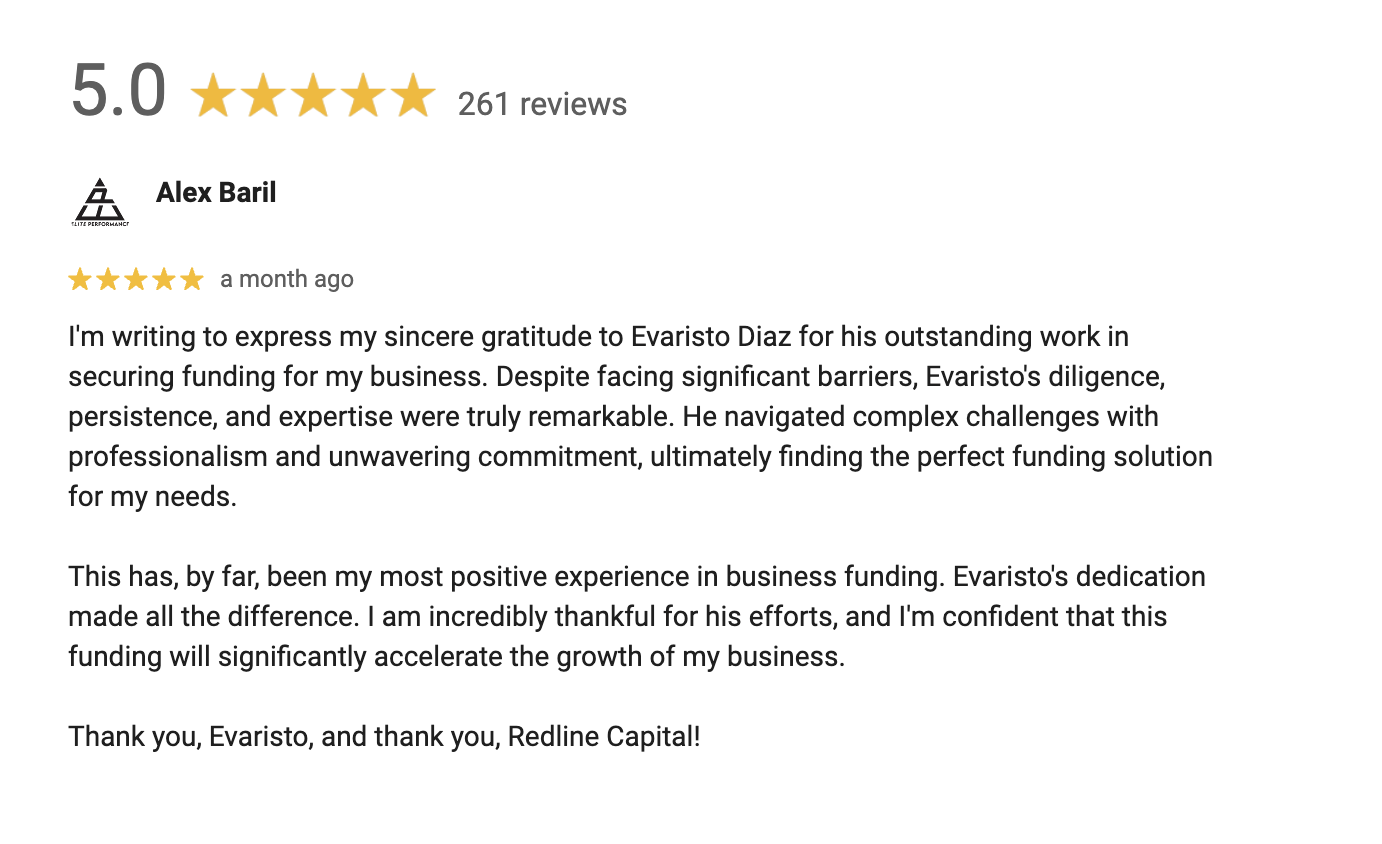

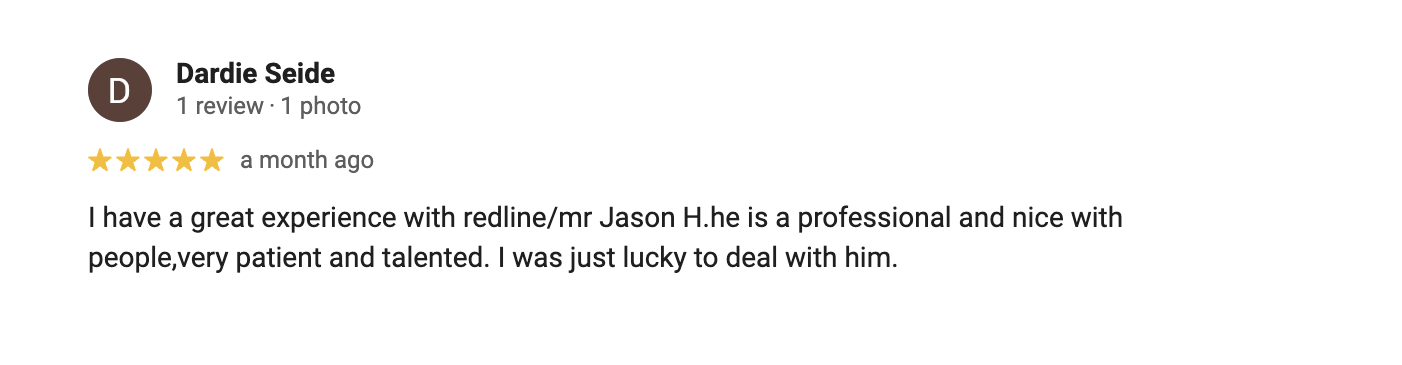

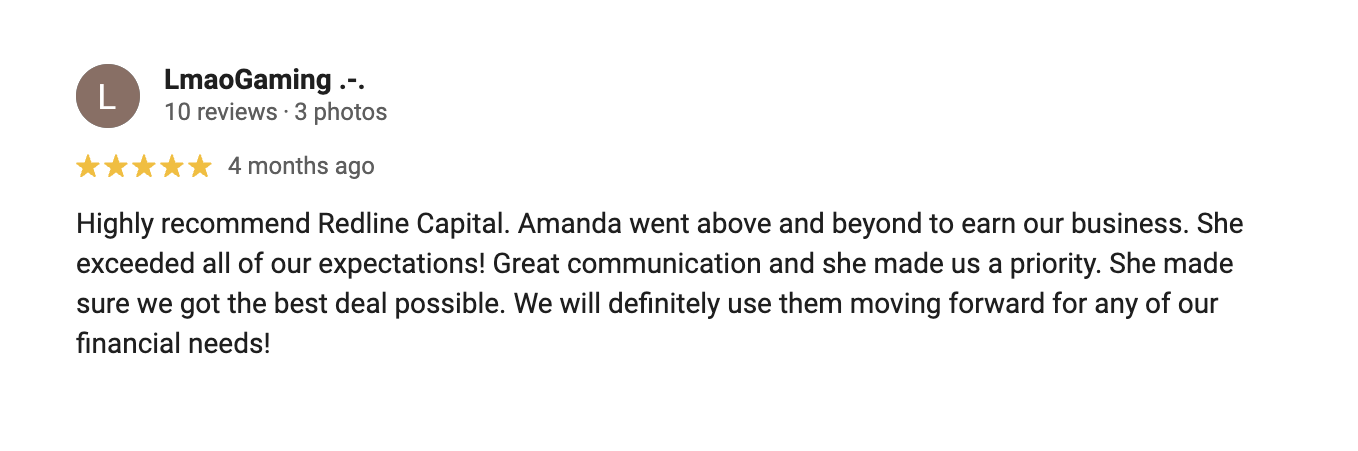

What Our Customers Have to Say

Here are a few reviews from our customers:

To hear from more of our customers, check out our case studies page:

Redline Capital offers fast and flexible revenue-based financing. Get in touch with our team to receive a tailored quote based on your business.

6 Additional Revenue-Based Financing Companies

We think you can get the best offers for your business with Redline Capital, but we still encourage you to shop around. Get a few more offers from other revenue-based companies, and then you can pick the best option for your business.

2. Lendio

Lendio connects business owners with 75+ lenders through its integrated technology platform. This platform uses an advanced algorithm and AI to match businesses with the right financing option and lender. Small businesses can quickly and easily find short-term working capital products, including MCAs. Plus, you can customize which lenders and financing types are shown to you based on your borrowing comfort level.

3. National Business Capital

National Business Capital offers entrepreneurs MCAs, lines, and term loans in addition to revenue-based financing. They offer a business advisor who will help you choose the right funding for your needs and connect you with the right lender. National Business Capital can help companies with funding for transportation, equipment, payroll, and more.

4. Credibly

Credibly is a well-known direct lender that offers multiple small business financing options for small to mid-sized businesses, including business loans and lines of credit, cash advances, and working capital loans. They also operate a large ISO partner network, which opens up even more financing opportunities.

Besides your credit score, Credibly considers factors such as time in business and the financial habits of your company (e.g., how long you’ve maintained a business bank account) when determining what you’ll qualify for. They serve companies in many industries, including consulting, healthcare, fuel, landscaping, and retail.

5. Fundera

Fundera (acquired by NerdWallet) is a marketplace platform that uses technology to connect businesses to multiple lenders simultaneously with one application. This allows you to compare options on your own without talking to a representative. While this approach may be effective if you prefer to work independently, working with a reputable broker lets you tap into the expertise of someone who knows all the pros and cons of various lenders and financing options.

Eligibility criteria will vary depending on the product and lender; generally, they look at business and personal credit scores, time in business, and revenue.

6. United Capital Source

United Capital Source can connect businesses across 250+ different industries with 75+ different lenders to secure funds of $5k to $5m. They focus on high-volume ISO, so businesses must have annual revenue of over $120k, have been established for more than 4 months, and have a credit score of 525+. Although they’re known for transparency, they don’t readily share repayment terms upfront, so you’ll have to apply for those specifics.

7. Fundmates

Fundmates offers revenue-based financing exclusively for YouTube creators. For repayment, they only take a percentage of your AdSense revenue, typically between 20% and 50%. Fundmates can lend between $30k and $1m, with term lengths of 6–24 months.

Beyond financing, Fundmates also offers additional tools and services, including video editors, thumbnail designers, and free MCN access.

Frequently Asked Questions

What Is Revenue-Based Financing?

Revenue-based financing is a type of funding where businesses receive capital in exchange for a percentage of their future monthly revenue. Unlike traditional loans, there are no fixed repayment schedules. Instead, payments fluctuate based on how much revenue your business generates each month.

Additionally, this type of financing is typically easier to get because the application process doesn’t require tons of legal or financial documents, a high credit score, or consistent profitability.

What Are the Advantages of Revenue-Based Financing?

Advantages of RBF include:

- Fast access to capital: The approval process is faster than seeking a bank loan.

- No fixed repayments: This gives you the flexibility to invest in growth without the pressure of paying fixed monthly payments.

- Non-dilutive: You will remain in control of your business. This is a major advantage over venture capital or equity funding.

- Freedom to use funds: This funding can be used for whatever your business needs.

- Static payoff amounts: Unlike traditional loans that come with a fixed interest rate that accrues over time, RBF has a set repayment amount — typically 1.1 to 1.4x the amount of funding.

What Are the Disadvantages of Revenue-Based Financing?

The disadvantages of RBF are:

- It can be expensive: The cost of capital in revenue-based financing can be higher than a traditional bank loan.

- You need steady revenue: Revenue-based financing suits companies with a consistent and predictable revenue. If your business has unpredictable or inconsistent revenue, this may not be the best option for you.

- The repayment periods tend to be shorter: If you’re looking for repayment periods over 12 months for a long-term project, it may be better to try a standard bank loan, a line of credit, or other funding options. RBF is ideal for short-term initiatives that increase revenue, which can be used to cover the flexible payments and repay the advance.

What Can Revenue-Based Financing Be Used For?

Revenue-based funding can be used for various purposes, including:

- Working Capital: Covering short-term cash flow needs, including paying suppliers or covering payroll.

- Inventory: Funding the purchase of new stock.

- Marketing: Supporting a marketing campaign to expand the business or enter a new market.

- Rent and Lease: Paying for physical space, including office and retail locations.

- Equipment: Purchasing specialized equipment.

- Employee Wages: Funding new staff.

- Funding New Initiatives: Supporting projects, such as developing new products, to increase revenue.

- Bridge Financing: Providing capital to bridge gaps between funding rounds.

Redline Capital offers fast and flexible revenue-based financing for companies in construction, health, retail, and more. Get in touch with our team to receive a tailored quote based on your business.